After discussing the chaos of the Great Depression and its economic fallout, in the last post we talked about the series of shocks to the economy that America occurred during the Great Moderation. Despite these shocks, the US economy remained resilient and avoided a major recession. Good times, right? Great news!

But…the good times always seem to end, and they finally did when the ’90s housing bubble grew so large (and fragile) that it eventually popped, leading to economic free fall.

The housing bubble

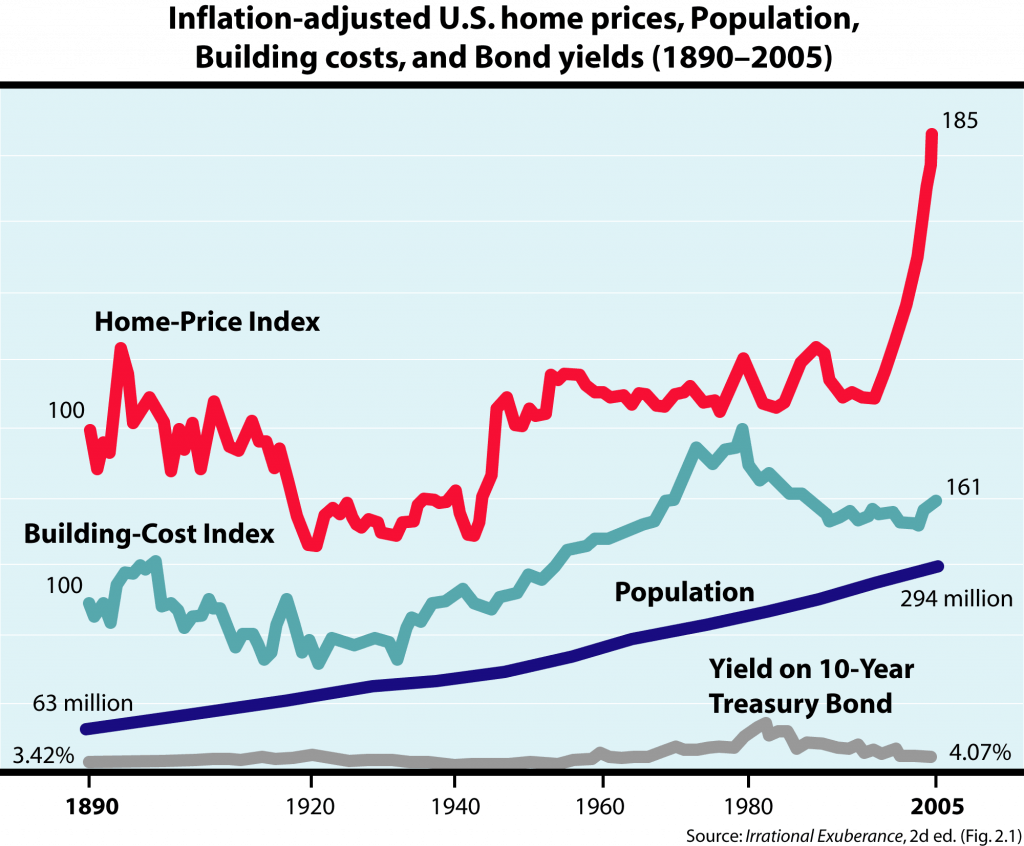

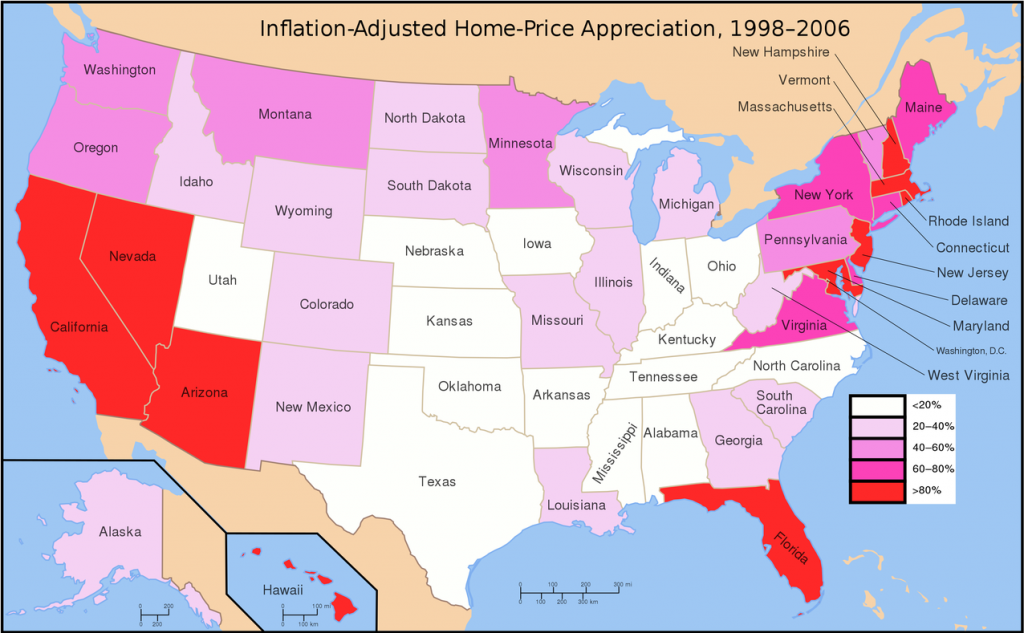

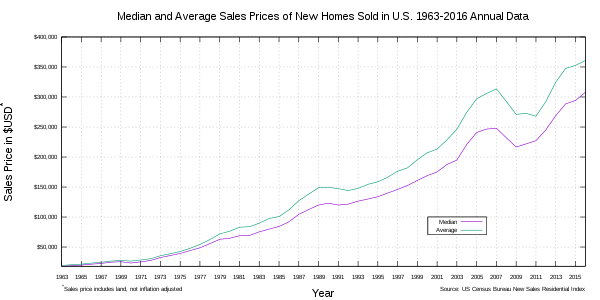

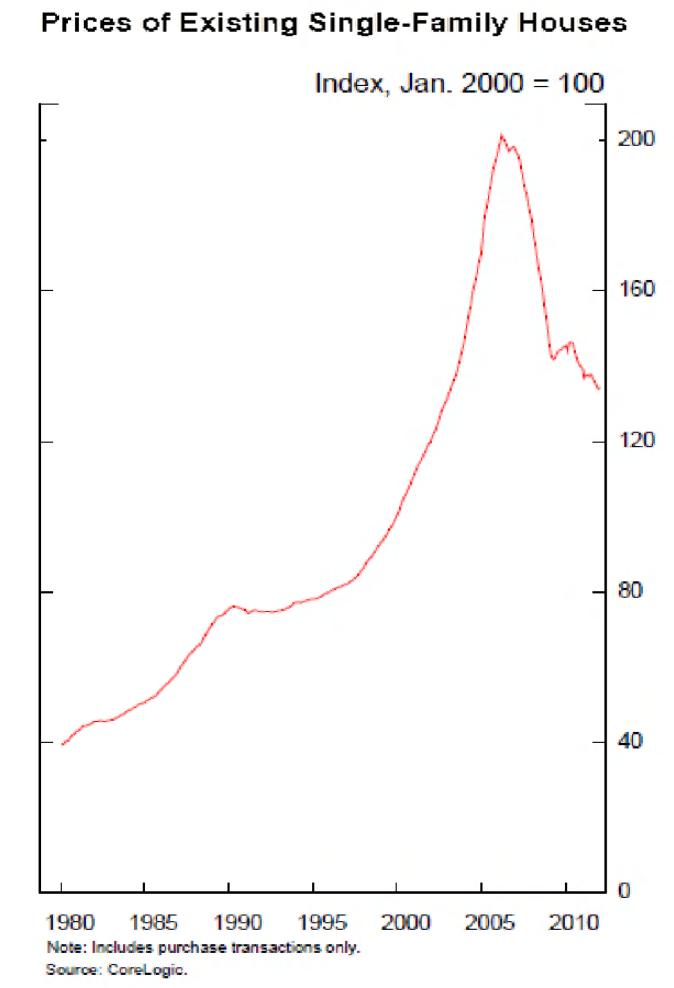

From the late 1990s until early 2006, house prices in the US soared.

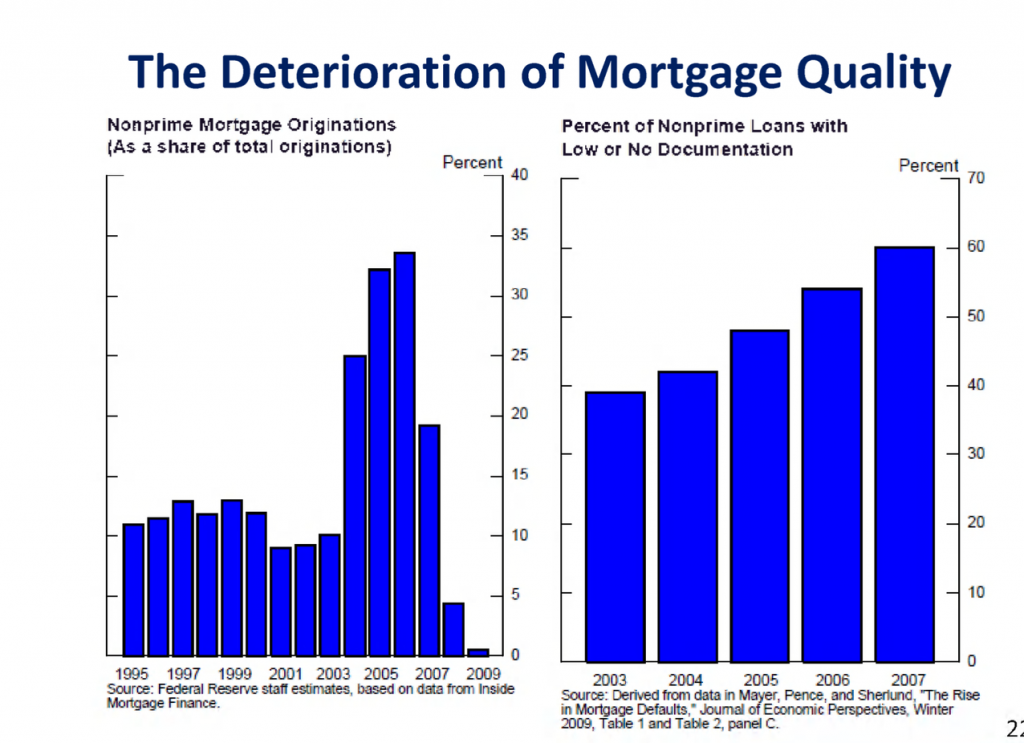

During this surge, mortgage lending standards deteriorated significantly and alarmingly. For example, in early 2000, the average subprime borrower had a FICO score of 660 or less. By 2005, the required FICO score dropped to 620. You can already see how this is heading for trouble.

Other examples of dangerous lending practices included:

Interest-only adjustable-rate mortgages (ARM): An “ARM” is when the interest rate varies throughout the life of the loan. An interest-only adjustable-rate loan is when a borrower is only required to pay the interest portion for a certain period of time, before the payments balloon at the end to pay off the actual loan. During the housing bubble, lenders offered “negative amortization ARMs,” where the initial payments did not even cover interest costs.

Long amortization: Lenders offered loans where the payment period was greater than 30 years.

No-documentation loans: Prior to the early 2000s, home buyers typically made a significant down payment (e.g., 10%, 15%, 20%) and had to document their finances in detail. This was a wise strategy on the part of lenders and prevented catastrophe. But as house prices rose, many lenders began offering mortgages to less-qualified borrowers and required little or no down payment and little or no documentation. Bad idea. Abysmal, in fact.

NINJA: No income, no job, no asset verification required (NINJA) mortgage products

This is just the tip of the iceberg in terms of the sloppy lending practices that persisted during the ’90s. As house prices continued to rise, the equity value on homes increased, which allowed borrowers to refinance into more-standard mortgages after a few years.

Rising house prices and weakening mortgage standards fed off each other and created a vicious cycle. As house prices rose, people had a sense of optimism, and so they poured all their money into buying homes.

On the flip side, lax lending standards drove the soaring demand for housing. Banks were too confident about house price increases and didn’t foresee a scenario where hundreds of people would default at once. If they ran into problems, banks assumed they could just sell their loans to riskier buyers. It was a vicious cycle, rapidly leading toward a devastating economic end.

When house prices stopped rising, borrowers could neither refinance nor meet the (typically increasing) payments on their exotic loans.

In addition to deteriorating lending practices, there were many other things happening in the economy that were leading indicators of the housing crisis, each of which we will briefly discuss below.

1) Securitized products

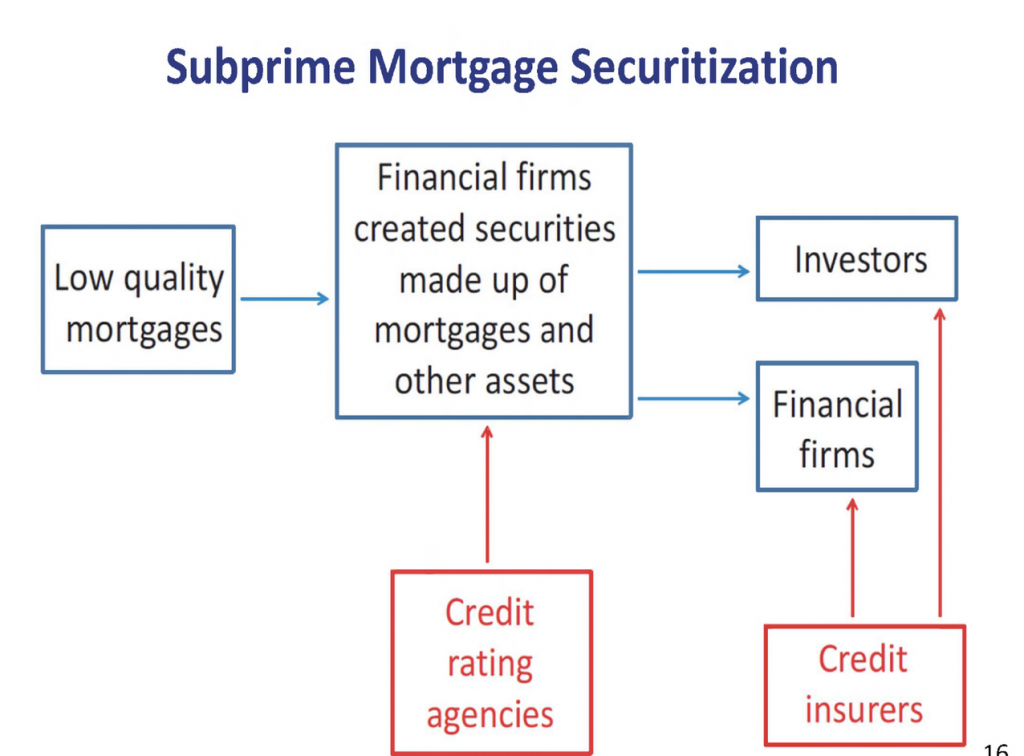

Another big factor that played into the housing bubble was a large international demand for US assets. Banks took advantage of this by creating securities that packaged exotic and subprime mortgages with better loan products and selling them to meet international demand and other investors (e.g., pension funds, accredited investors, etc). This process of bundling a bunch of assets into a new type of asset is known as “securitization.”

Some of these securities were very complex and opaque derivatives—for example, collateralized debt obligations, or CDOs.

Rating agencies gave AAA ratings to many of these securities.

And companies like AIG sold “insurance” to protect investors or financial firms that held these securities. These ratings masked the truth about the real risk underlying these securities.

2) Predatory lending

Predatory lending, which came to define the ’90s American economy, is when lenders entice borrowers to enter into unsafe loans for inappropriate purposes. Banks failed to adequately monitor and manage risks they were taking. If you were human, they gave you a loan.

Countrywide Financial, for example, was sued for using false advertising and deceptive tactics to push homeowners into complicated, risky, and expensive loans so that the company could sell as many loans as possible.

3) Community Reinvestment Act

The Community Reinvestment Act was established in 1977 to help low-income Americans get mortgage loans so they could own homes. This encouraged banks to relax their lending standards and lend to higher-risk families.

While the Act may has been well intentioned, its downstream effects were a recipe for disaster.

4) Low interest rates

Yet another trigger was low interest rates.

In 2001, Federal Reserve chairman Alan Greenspan dropped interest rates to 1% to help jumpstart the economy after the dot com bubble. Why does this matter? Because a lowered Fed Funds rate impacts mortgage rates as well. Mortgage rates are set in relation to 10-year treasury bond yields, which, in turn, are affected by Federal Funds rates.

A drop in interest rates reduces the cost of borrowing, which then increases demand. Hence, house prices increased significantly, with inflation-adjusted US home prices increasing 5% during this period.

Former Federal Reserve Board Chairman Alan Greenspan later admitted that the housing bubble was “fundamentally engendered by the decline in real long-term interest rates.”

5) Lack of regulation and deregulation

Another key trigger was the lack of proper regulation and supervision. Despite the fact that financial institutions were recklessly taking on too much risk, the Federal Reserve failed to regulate them.

For example, starting in the 1980s, there was a lot of deregulation in the banking industry. The Depository Institutions Deregulation and Monetary Control Act of 1980 allowed similar banks to merge and set any interest rate. The Garn–St. Germain Depository Institutions Act of 1982 allowed adjustable-rate mortgages. The Gramm–Leach–Bliley Act of 1999 allowed commercial and investment banks to merge. In essence, the deregulation allowed banks to get really big without also increasing Fed supervision in tandem.

To add to the trouble, in 1997, Greenspan fought to keep the derivatives market unregulated. Eventually, the U.S. Congress under President Bill Clinton allowed the derivatives market to be self-regulated. This led to a huge surge in the derivatives market (explained below).

The CDS and CDO damage

A popular derivative product sold during this time was credit default swaps (CDS). A credit default swap is when a seller and buyer hedge their bets based on an underlying reference asset (e.g., a mortgage). The seller of the CDS insures the buyer against the asset defaulting. The buyer of the CDS makes a series of payments to the seller. If the reference asset defaults, the buyer receives a payoff from the seller. Otherwise, the buyer ends up paying the seller the payments until the maturity date.

So as an investor, instead of lending directly to the borrower, you now could sell credit default swaps and insurance against those same borrowers defaulting. In both cases, you got monthly payments—if you lent directly to the borrower, you earn interest payments, whereas if you sell a CDS, you receive an insurance payment.

In both cases, you lost money if the borrower defaulted. But the key difference between lending directly to the borrower versus selling CDS is that an unlimited number of CDS could be sold against a single mortgage, and a lot more money could be made.

The logical conclusion, then, is that the CDS market exploded. The volume of CDS increased a hundredfold from 1998 to 2008. At the end of 2001, there was $920 billion in credit default swaps outstanding. By the end of 2007, that number grew to $62 trillion. Yes, trillion.

Even worse (yes, it keeps getting more awful!), rating agencies used the Copula formula to assign risk to these assets. The formula, created by David Li, was thought of as a breakthrough for assigning risk to underlying assets. As you might know, analyzing the underlying risk of an asset is an incredibly complex process. If it were as easy as a plug-and-play formula, we’d all be billionaires.

But at the time, the collective delusion was too high for any rationality to matter. Ratings agencies assumed they could rely on this simplistic formula, regardless of how complex the underlying assets were. For example, rating agencies at the time were giving triple-A ratings to collateralized debt obligations (CDOs). A CDO is an incredibly complex financial product that pools together corporate bonds, bank loans, mortgage-backed securities, etc. and then is sold to institutional investors. Financial institutions used the Copula formula to price the risk of CDOs, which was in essence a false guarantee to the buyers of the CDOs. As a direct result, the CDO market ballooned from $275 billion in 2000 to $4.7 trillion by 2006.

Calculating the risk of these complex derivatives cannot be narrowed down to a simple formula, and yet it was. The financial gurus were making too much money for anyone to convince them otherwise. Plus, house prices were still going up, so there was no reason to be pessimistic.

This was fine when things were going “well,” but the good times eventually came to an end. It’s no wonder Warren Buffett famously referred to derivatives as “financial weapons of mass destruction” in early 2003.

6) Fannie Mae and Freddie Mac

At the time, there were federal mandates in place to promote affordable housing. Fannie Mae and Freddie Mac are private corporations established by the Congress to help create affordable housing for Americans. The two entities are referred to as government-sponsored enterprises (GSEs). They don’t issue mortgages; rather, they’re the largest “packagers” of individual mortgages into mortgage-backed securities (MBS), which they guarantee against loss (hint: the government sponsors them).

The Housing and Urban Development Act of 1992 mandated Fannie Mae and Freddie Mac to have at least 30% of their total loan purchases be related to affordable housing. By 2005, 52% of the loans Freddie and Fannie issued were to borrowers with income that was less than the median in their area. To meet these mandates, they loosened their lending standards and loaned money to people who couldn’t, in actuality, afford to buy homes. Fannie Mae and Freddie Mac bought $200 billion in subprime mortgages from banks and engaged in massively risky loan purchases. To compound an already bad situation, they were operating with inadequate capital to back their guarantees. This is not looking good…

7) Housing tax policy

In 1997, the Taxpayer Relief Act of 1997 created a $500,000 exclusion of capital gains on the sale of a home for married taxpayers (and $250,000 exclusion for single taxpayers), which could be used every two years. All other capital gains exclusions were removed, and housing became the only investment that escaped capital gains tax. This encouraged people to buy homes instead of other assets like stocks and bonds.

This built on the unequivocally American belief that owning a home is the ultimate dream and that renting is a waste of money. Further sweetening the poisoned financial pie, the media did a spectacular job promoting home ownership and real estate as great investments. Combined with cheap capital and tax advantages, this led Americans to buy homes and investors to speculate on the mortgage market at an unprecedented rate.

8) Dot-com bubble collapse

Remember the dot com crash in the last post? When the stock market crashed, many people started to move their money out of speculative stocks and into speculative real estate. Humans do so love to speculate 😉

Home-ownership soared

In summary, as a result of all of the reasons above (and more that I did not list, such as over-leveraging, huge growth in shadow banking, etc.), Americans started buying homes left and right. From 1990 to 1995, an average of 609,000 new single-family houses were sold. By 2005, that number went up to 1,283,000. And during this period, house prices appreciated a lot.

The bubble pops

Yep. You knew it was headed in this direction. The financial party couldn’t last forever (by now you know they never do). Eventually, rising costs of homeownership began to dampen housing demand, and house prices began to drop in early 2006.

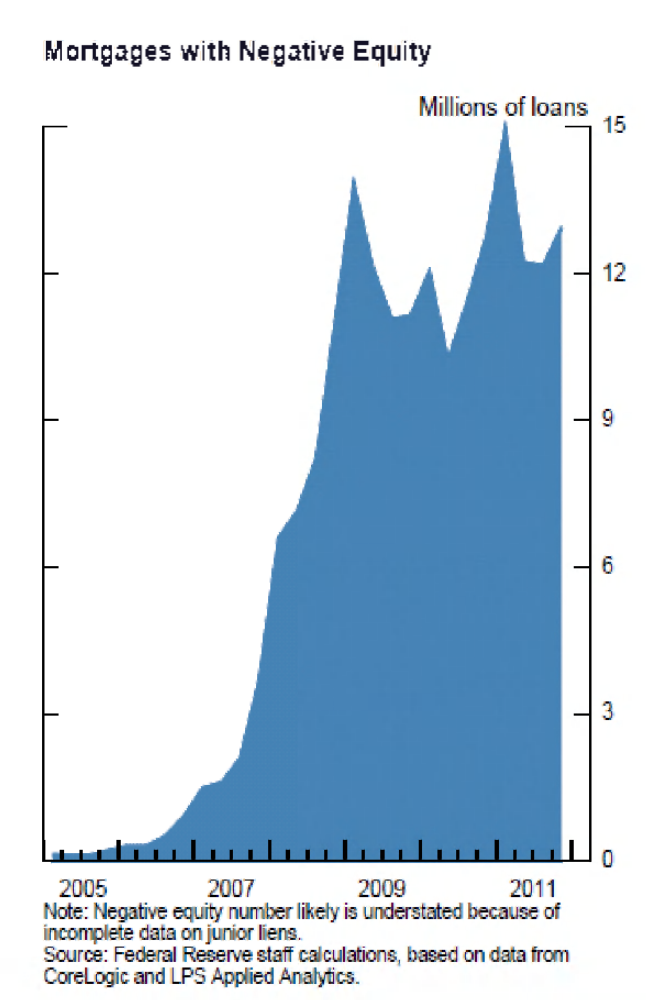

As house prices fell, people owed more on their mortgages than what their houses were worth, and people were suddenly underwater (also known as “negative equity”).

Homes became less affordable. Mortgage payments as a share of income rose sharply.

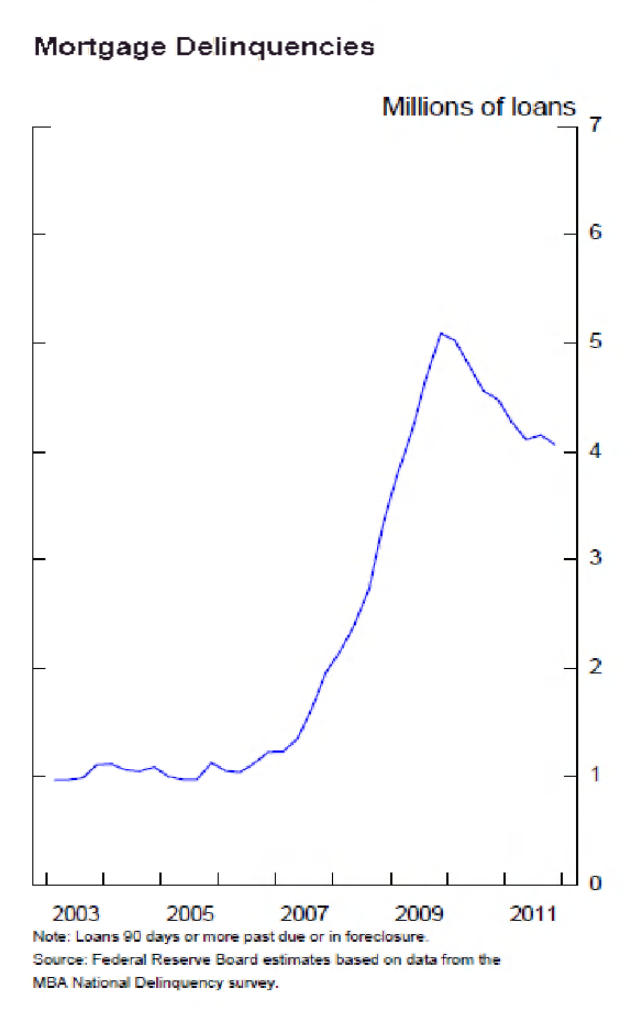

The banks that serviced these toxic mortgages and mortgage-backed securities started to face massive losses.

“The great housing bubble has finally started to deflate… In many once-sizzling markets around the country, accounts of dropping list prices have replaced tales of waiting lists for unbuilt condos and bidding wars over humdrum three-bedroom colonials.”

Fortune magazine, May 2006

Given how big the housing market had gotten during this period, any signs of collapse were seen as a massive risk to the overall economy. The US economy had been resilient for the last couple of decades, but the collapsing housing bubble would be too big to contain.

By March 2007, more than 25 subprime lenders declared bankruptcy. The biggest one was IndyMac Bank. IndyMac had given out really risky loans to borrowers and even went as far as to fabricate the volume of credulous loans that it gave out to make the situation seem better than it was. But when home prices declined, they couldn’t hide from their bullshit much longer. What came next was a catastrophic bank run and eventual bankruptcy. IndyMac was one of the largest bank failures of the ’90s… and it was just one of many.

Things got really ugly, really quickly. In the next post, we’ll learn more about the “pop” and the collapse that followed. (I’ll give you a hint – it’s not nearly as pretty as an imploding soap bubble.)

Add Comment