By now you understand, based on all the previous posts, that the Fed’s core responsibility is to prevent financial panics and/or come to the economic rescue as needed. The panic of 2008 threatened the stability of the global financial system at large, necessitating a large-scale intervention by the Fed.

In this post, we will take a look at some of the different things the Fed did to carry out its duties and help calm matters in 2008.

Special liquidity and credit facilities

Recall that one of the Fed’s primary roles is to be a lender-of-last-resort when banks and financial institutes are failing. Lending freely to failing banks is intended to help halt bank runs and restore the market. In 2008, the Fed worked closely with the Treasury and other regulatory agencies, such as the FDIC and SEC, to provide liquidity to firms that were failing.

The Fed launched a series of different funding programs that you can read about in detail here. In essence, the Fed loaned money out to thousands of struggling financial institutions and businesses that used their solvent assets as collateral to secure the loans. Since all the loans were collateralized, the risk of defaulting was believed to be low.

Moreover, the Fed also coordinated with foreign central banks to help the international markets, which were coming under a lot of pressure. The Fed provided temporary foreign currency swaps, meaning it gave dollars to other central banks in exchange for foreign currencies. These swaps allowed foreign central banks to fund their investments in dollar-denominated assets. The foreign central banks agreed to buy back their own currency at a specified future date at the same exchange rate that was used to make the original currency swap.

Overall, the lending programs were effective in stopping bank runs on various types of financial institutions. The programs also helped to slowly restart the flow of credit in the markets, which helped calm the panic.

As the financial system calmed down, it was no longer economically appealing for institutions to borrow from the Fed, so they naturally wound down on their own. The loans that the Fed gave out were eventually repaid in full, with interest.

All the 2008 lending programs that the Fed launched were phased out by March 2010.

Supporting critical institutions Bear Stearns and AIG

The Fed also helped bail out large financial institutions such as Bear Stearns and AIG.

Bear Stearns

Bear Stearns, one of the largest financial institutions in the world, was on the brink of failure in 2008. If Bear Stearns collapsed, it would only exacerbate the dire economic situation.

J.P. Morgan’s willingness to buy out Bear Stearns gave the Fed some confidence that perhaps Bear Stearns remained solvent. For that reason, the Fed facilitated a loan for J.P. Morgan to take over Bear Stearns.

AIG

AIG is a multinational insurance and financial services firm that was facing serious liquidity problems in 2008 and was on the brink of failure. AIG sold insurance on bad mortgage-related securities, and when the mortgage market fell, everything (predictably) came crashing down.

Given that AIG was interconnected with many other parts of the global financial system, if the firm failed, it would have had a massive effect on the global financial market and global economy.

In order to prevent collapse, the Fed loaned AIG $85 billion in October 2008, using AIG assets as collateral. The Treasury subsequently lined up a $182 billion bailout for a 53% stake in the company.

Overtime, AIG stabilized and repaid the Fed with interest. The firm has since made progress in reducing the Treasury’s stake in the company.

Bad taste in everyone’s mouth

The bailout of AIG and Bear Stearns was not viewed as a positive by the public. For one, other companies that failed during the crisis weren’t rendered assistance, and this was viewed as unfair (because let’s face it, it is). Moreover, bailouts like this create very perverse incentives because if these large financial juggernauts know that they will be bailed out when things go south, they are not incentivized to use best practices and will instead continue to take dangerous risks.

However, the Fed and US Government felt that if the whole system collapsed, it would have a very serious impact on the US and global economy. Regardless of public perception, they felt this was the best way to right a sinking ship.

The problems at Bear Stearns, AIG, and other large financial institutions highlighted the need for a better way to deal with massive financial institutions that were on the brink of failure (hint: having a system where companies don’t get “too big to fail” in the first place).

Stress-testing financial institutions

Another way the Fed came to the rescue in 2008 was by leading stress tests of big banks in the US. The idea was that stress-testing the banks would give investors some confidence about these banks’ solid economic viability. In spring of 2009, the Fed led tests on 19 of the largest U.S banks.

These stress tests helped restore some investor confidence and allowed these banks to raise about $140 billion in private capital (rather than relying completely on the Fed and government for bailouts).

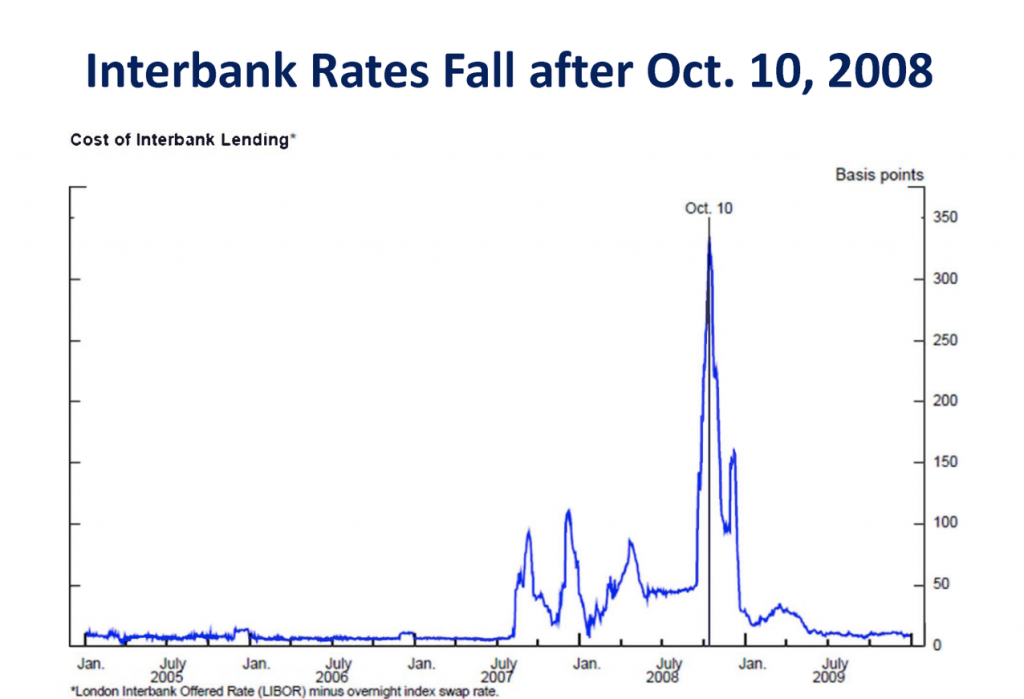

Reducing interbank rates

Another approach to helping calm the panic was to lower interbank rates, the interest rates banks pay to borrow short-term funds. On October 10, 2008, all of the G-7 countries agreed to work together to make this happen.

Reducing federal funds rate

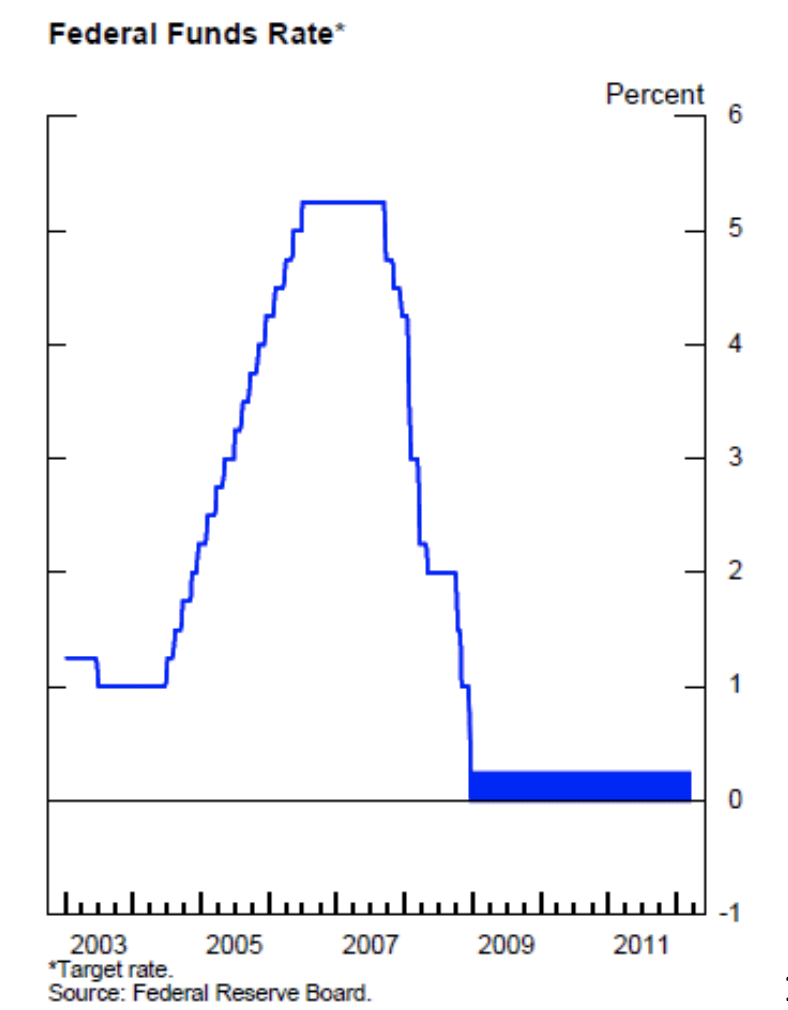

As we learned in previous posts, the Fed lends to banks through a discount window. During the crisis, the interest rate (i.e. Fed funds rate) on discount window loans was drastically reduced. To make sure banks always had access to funds and prevent any potential panics, the Fed reduced the federal funds rate from 5.24% in September 2007 to nearly zero in December 2008.

Large-scale asset purchases (i.e., QE)

Despite dropping the federal funds rate to nearly zero, the economy was not recovering. However, the Fed had exhausted what it could do with monetary policy because the short-term interest rate was already nearly 0%. When interest rates are at zero, it creates a “liquidity trap” where people prefer to hold cash or very liquid assets because the return on lending their cash is so low. Therefore, the economy is at risk of entering a deflationary cycle where wages and prices fall.

The Fed, therefore, needed a plan B badly. Since lowering short-term interest rates to nearly 0% to help open up credit for large banks was not enough to induce a recovery, the Fed then sought out a way to reduce long-term interest rates (e.g., mortgages, corporate bonds, etc) as well.

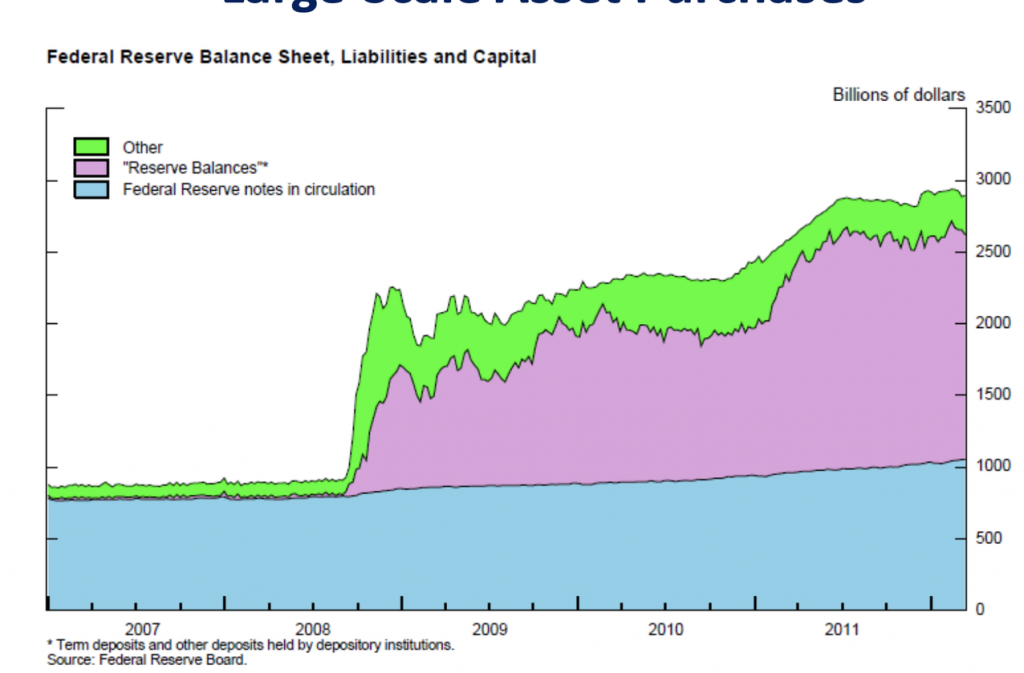

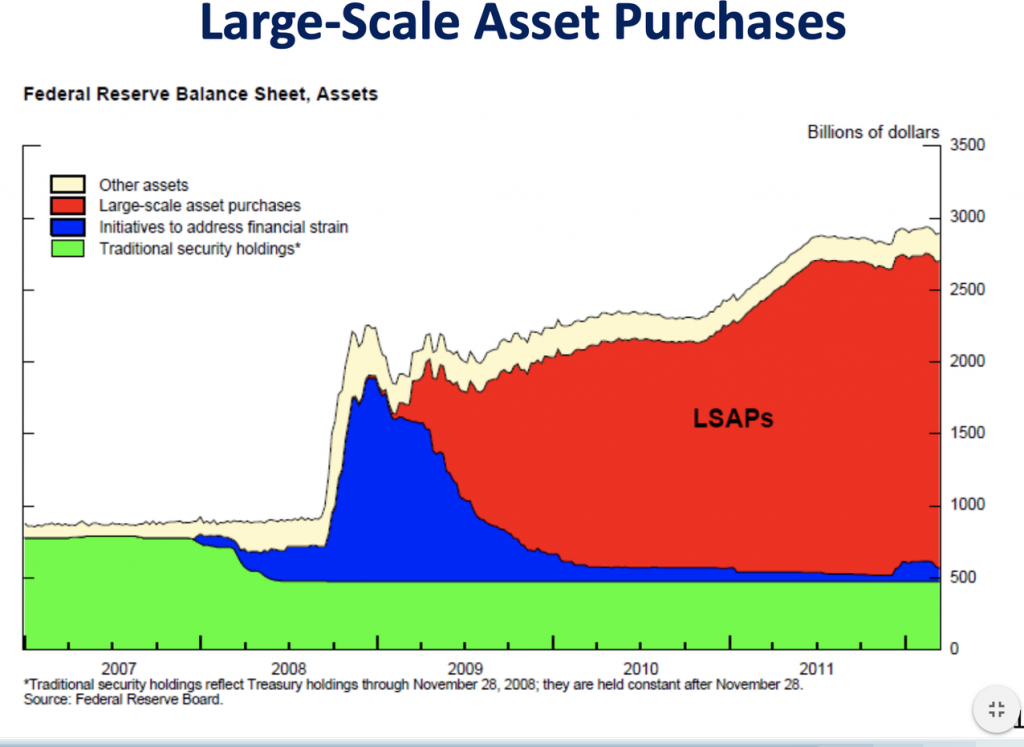

In order to influence longer-term interest rates directly, the Fed decided to buy ample Treasury and government-sponsored enterprise (GSE) mortgage-related securities. This became known as “quantitative easing.” The more technical term for this is “large-scale asset purchases” (LSAPs).

The idea behind LSAPs is that when the Fed buys Treasuries and GSEs, it reduces the supply of these assets. Economics 101 tells us that if the supply goes down, then demand goes up. By buying up these securities, the Fed creates demand from investors, who are both willing to hold these securities and to accept lower yields.

With a lowered supply of Treasury and GSE securities, investors also started to purchase other assets like corporate bonds. This increased demand (and reduced supply) of corporate bonds reduced the yields on these assets as well.

The intended goal of reducing long-term interest rates was attained.

It’s interesting to understand how the Fed paid for all this. The Fed doesn’t have the funds to purchase these assets outright. Contrary to a common misconception, the Fed is NOT printing money willy-nilly to engage in quantitative easing. Instead, it credits the accounts of the banks banking with the Fed. This increases the amount of reserves that banks have. In other words, they purchase the assets with digital money and therefore do not affect the amount of money in circulation. Instead, they increase the digital balance of reserves in banks.

Overall, the LSAPs that happened between 2009 to 2010 boosted the Fed’s balance sheet by more than $2 trillion.

There is often a misconception that LSAPs are government spending. However, this is not the case either. The government uses fiscal policy (i.e., taxation) to acquire funds. In this case, the central bank uses “monetary policy” to engage in LSAPs.

The assets that the Fed purchased are ultimately sold back into the market. In fact, the Fed makes a profit on these LSAPs.

From 2008 to 2011, the Fed made $200 billion in profits through LSAPs, which were transferred to the Treasury (which arguably reduced the federal deficit).

Did LSAPs work?

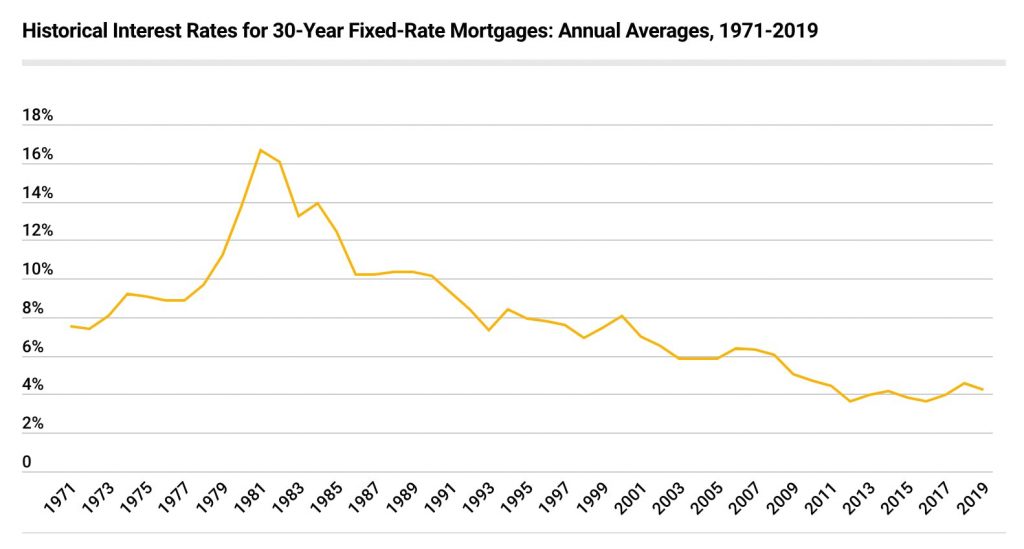

LSAPs seemed to have lowered long-term interest rates. For example, 30-year mortgage rates fell below 4% after 2008.

Corporate bonds’ yield also fell, which allowed businesses to get credit more easily.

Did the economy recover though?

We could spend weeks (more likely months) analyzing the details of the Great Recession and the economy’s eventual recovery. For the sake of time, I will not go into that (because we need to get to the crypto part already!)

But I felt it was important for you to understand the types of actions that the Fed and government sometimes take to keep the economy afloat.

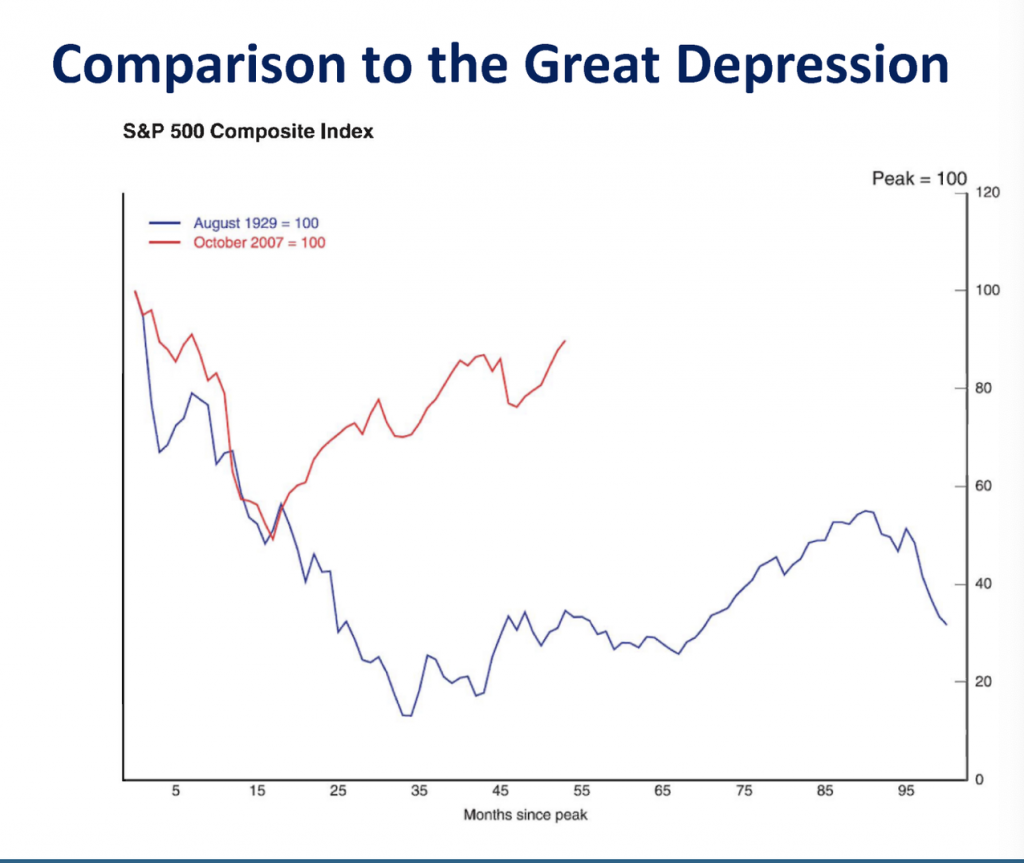

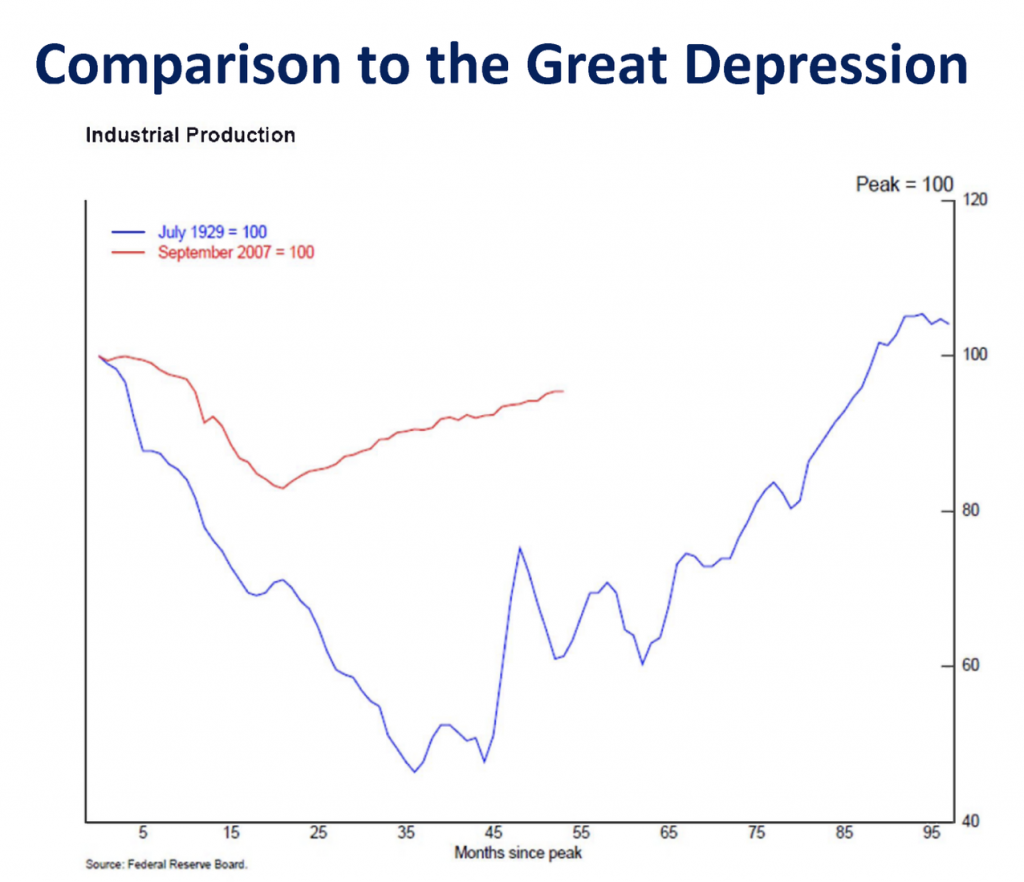

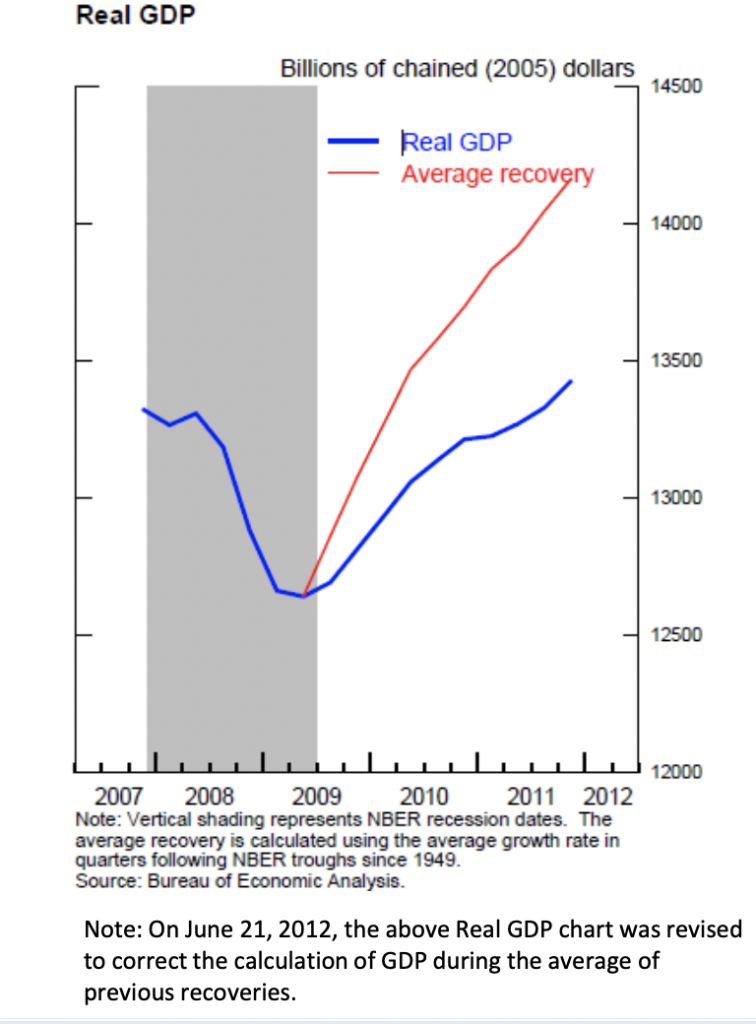

Overall, there is still a lot of controversy about what worked in 2008 and what didn’t. For better or worse, the Fed’s bailout actions likely did prevent the economy from reaching Great Depression levels.

However, who knows what would have happened if the Fed did not come to the rescue through quantitative easing. Would the story of the US have looked like Japan after the country’s bubble popped in 1991, and the economic recovery never really arrived?

Or would the market have eventually recovered to its pre-recession highs after a painful recovery period?

I will leave it up to you to ponder that particular mystery.

Satoshi designed Bitcoin such that no central entity can create Bitcoin outside of the strict schedule is a reaction to the current monetary system, which can create money at will. You can read more about it here.

Add Comment