By now we have spent a great deal of time understanding how the housing bubble got so big that it eventually popped.

What came after the pop was the most severe recession the US has endured since the Great Depression.

The crisis

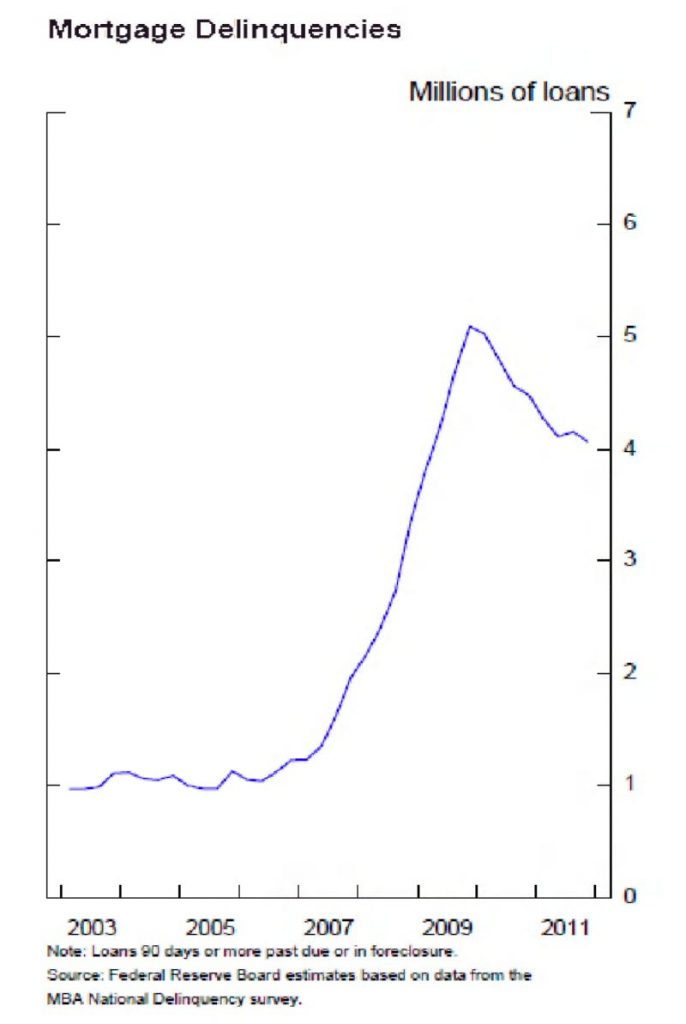

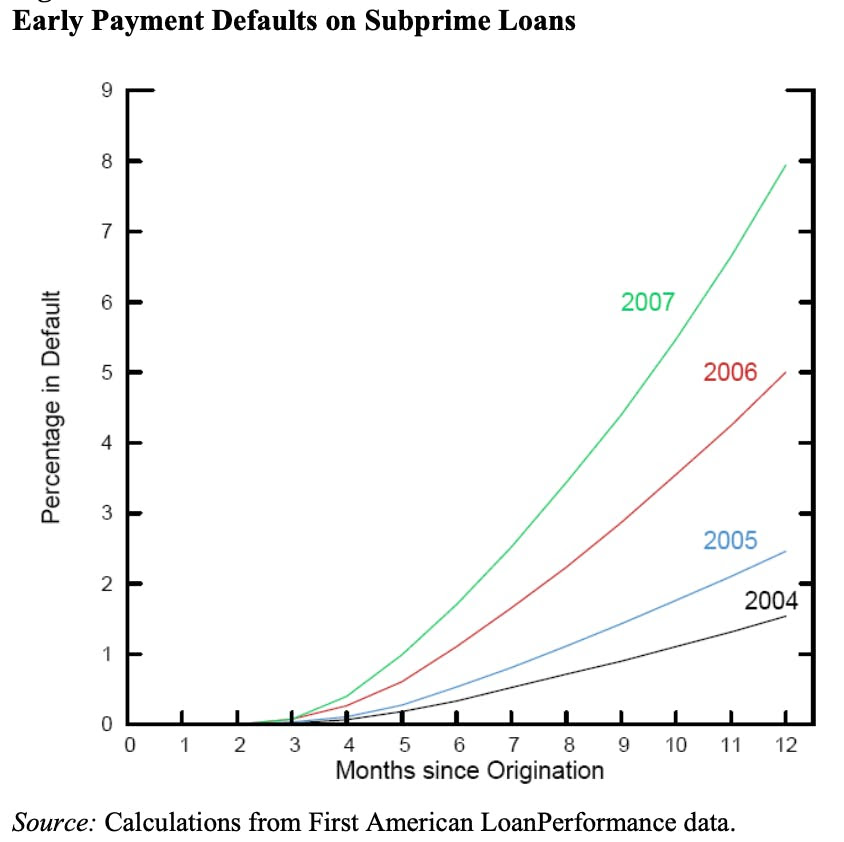

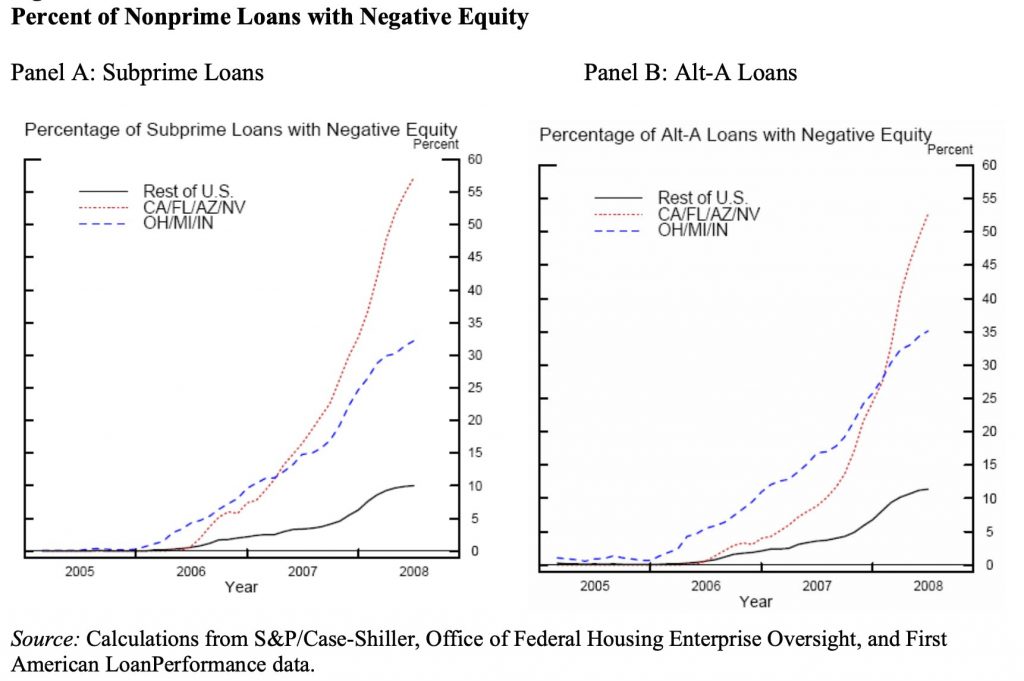

During the Great recession, the default rate on mortgages skyrocketed, resulting in many foreclosures.

Recall that a financial panic is when providers of short-term credit (i.e., depositors in a bank) suddenly lose confidence in the ability of borrowers (i.e., banks) to repay a loan. Once short-term creditors lose confidence, they try to withdraw their funds as quickly as possible.

As the value of mortgage-backed securities declined in 2008, buyers evaporated, and banks who were heavily invested in these assets suddenly faced a crisis. As house prices fell, it became clear that mortgage-related securities were on the verge of tanking.

However, it was unclear where the losses would fall because of how complex the financial market had become (we will see an example below).

Soon enough, bank runs began as investors started pulling their money from any firm they thought was vulnerable to losses. This created enormous pressure on big financial firms.

Some of the large financial firms that came under intense pressure in 2008 included:

Bear Stearns, which ended in a forced sale.

Fannie and Freddie Mac, whichwas placed in conservatorship, meaning their liabilities would be guaranteed by the U.S. Treasury. The government felt this had to be done to prevent further worsening of the crisis. Countries all around the world held hundreds of billions of loans. A collapse of Fannie and Freddie would not end well for anyone.

Lehman Brothers, whichfiled for bankruptcy.

Merrill Lynch, whichwas acquired by Bank of America because it was going under.

AIG, which received emergency liquidity assistance from the Fed.

Washington Mutual Bank, whichwas closed by regulators and later acquired by JP Morgan Chase.

Wachovia, which was failing and then saved by the acquisition of Wells Fargo.

This is just the tip of the iceberg. There were a LOT more bank failures and madness, which we won’t have time to get into in this post.

This was very different from the Great Depression because in the 1930s, it was mostly small independent banks that failed. In 2008, the banks were much bigger and far more intertwined.

To better understand this, let’s look at an example of how the failure of Lehman Brothers caused the entire financial economy to collapse on itself.

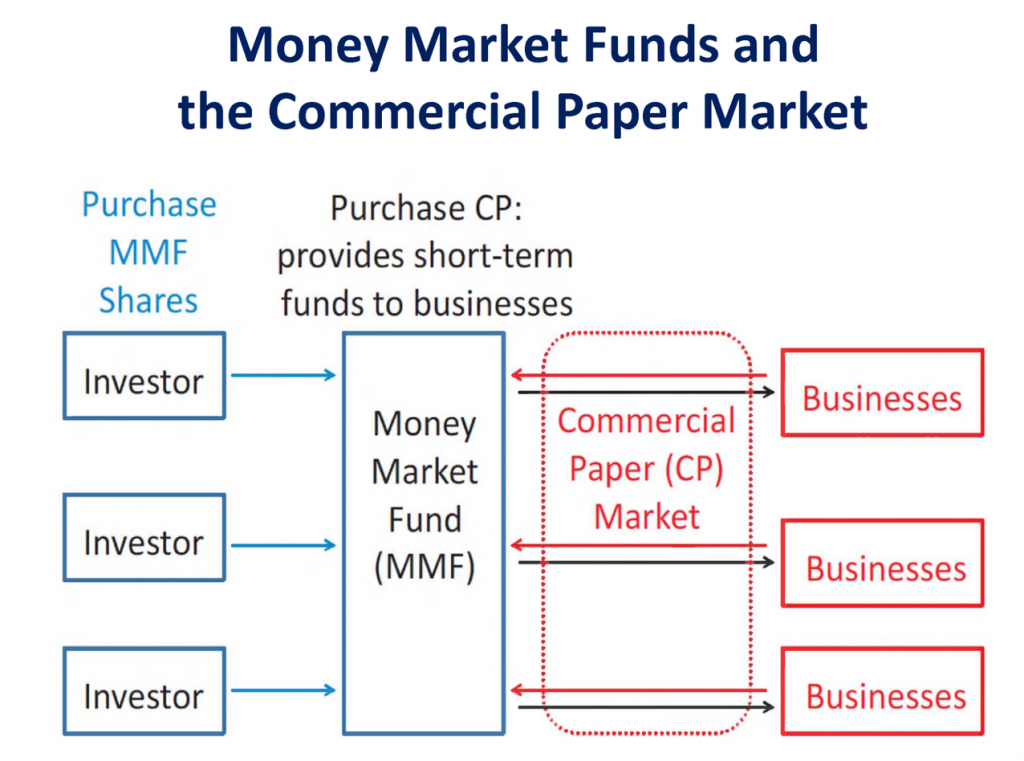

Money market funds and commercial paper market

Money market funds (MMFs) are companies that invest in highly liquid, near-term assets (e.g., commercial paper, cash, cash-equivalents, short-term debt instruments, etc.) and then sell shares of their investments to buyers.

MMFs historically have almost always maintained stable $1 share prices.

Although MMF shares are not insured, they are still considered extremely low-risk on the investment spectrum. Investors use MMFs like checking accounts and expect to be able to earn interest and redeem shares on demand for $1.

One common asset that MMFs invest in is commercial paper (CP). CP is a short-term (typically 90 days or less) debt instrument that companies issue and then use to pay for immediate expenses such as payroll and inventories. Financial institutions use CP to raise funds that they then lend to ordinary businesses and households.

The Lehman Brothers catastrophe

Lehman Brothers was a global financial services firm that was once considered the gold standard financial firm. During the 2000s, Lehman invested extensively in mortgage-related securities and commercial real estate and relied on CP to fund these investments.

But as the housing market started to collapse on itself, Lehman’s mortgage-related investments started to show massive losses. Lehman’s creditors lost confidence and started to withdraw their money from the fund. The losses were so big that Lehman could neither find new capital (because people lost faith in the firm) nor could they find another firm to acquire it.

On September 15, 2008, Lehman filed for bankruptcy, sending a massive shock throughout the financial system.

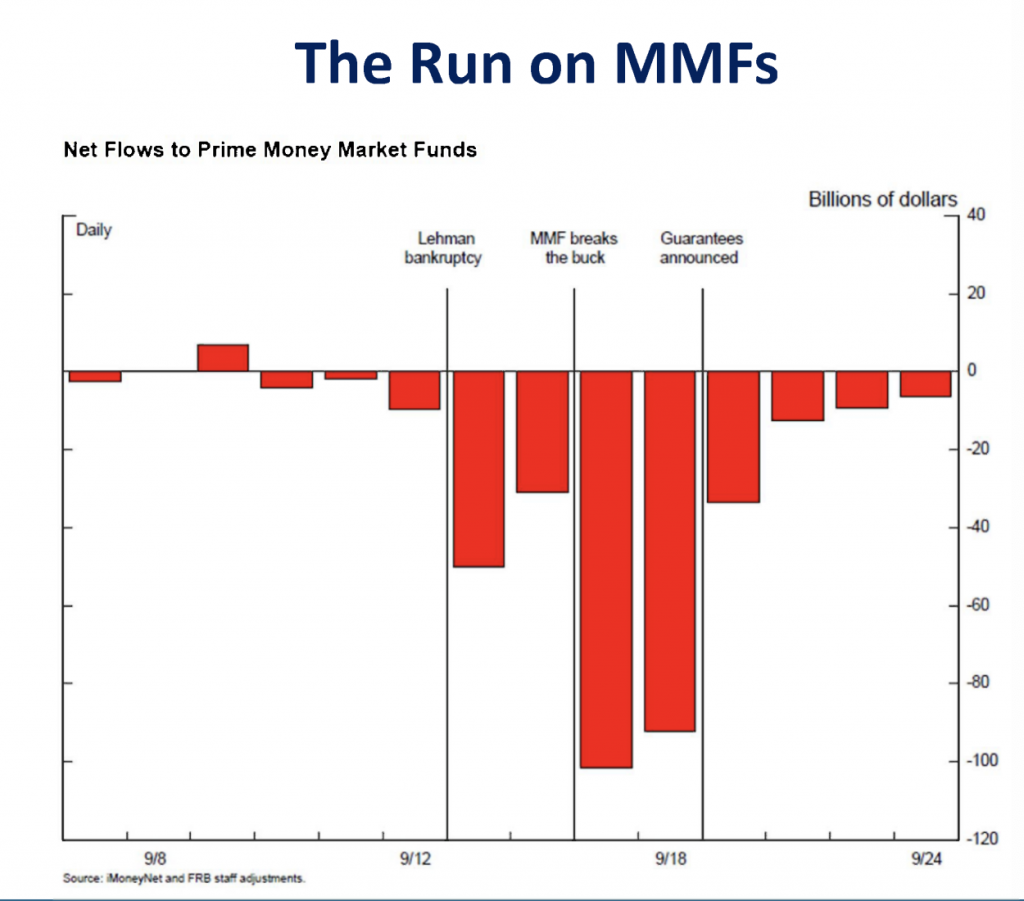

The Run on MMFs

After the collapse of Lehman Brothers, one of the many MMFs that issued CP to Lehman failed to maintain a $1 share price. This had a cascading effect on other MMFs because investors started to lose confidence in MMFs and rushed to redeem their money.

Seeing the crisis brewing, the Treasury offered a temporary guarantee of the value of MMF shares.

Also rendering assistance, the Fed created a program to provide emergency liquidity by lending to banks, which in turn provided cash to MMFs by purchasing some of their assets.

The combined efforts of the Treasury and the Fed helped to eventually cease the run on MMFs, but it took time.

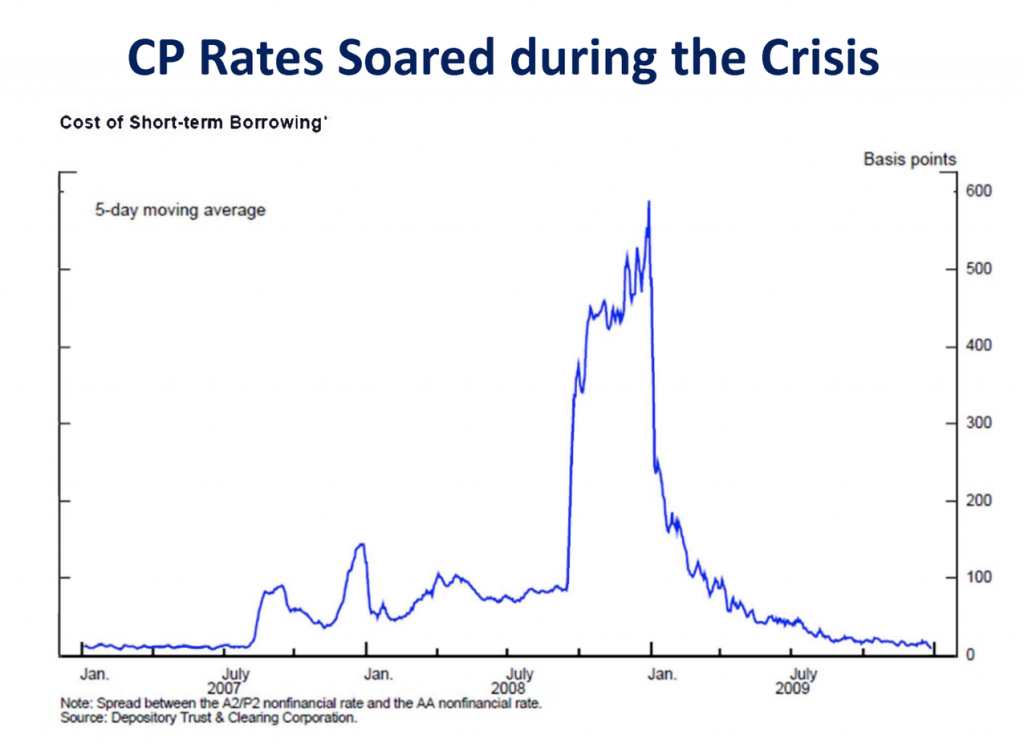

The CP market started to fall apart

The MMFs responded to the run on MMFs by curtailing their purchases of commercial paper. As a result, the demand for CP dried up, and interest rates on CP soared. This meant the cost of credit went up, which affected both businesses and households.

So in effect, the collapse of Lehman led to a run of MMFs, which then led to CP markets drying up, which had dire consequences on businesses and households. This is an example of a financial crisis caused due to interconnected financial systems. When everything is intertwined, if one thing goes wrong, a domino effect is never far-off from happening.

The Federal Reserve established special programs to repair functioning in the CP market and restart the flow of credit (which we will talk about in the next post).

The crisis spread around the world

The US represented over one-third of the global consumption between 2000 to 2007. Thus, the world depended on US consumer demand, and therefore the economic crisis that started in the US rapidly spread globally.

Moreover, the toxic securities sold during this period were not just owned by US investors. They were also owned by international investors. Complex derivatives (e.g., CDOs) made the situation worse because these products create an even greater linkage between so many different parts of the financial system.

As markets started to collapse and firms started to deleverage, international trade declined and developing countries saw their growth tank.

It was not a pretty scene at all. Cue the splat.

Economic consequences of the crisis

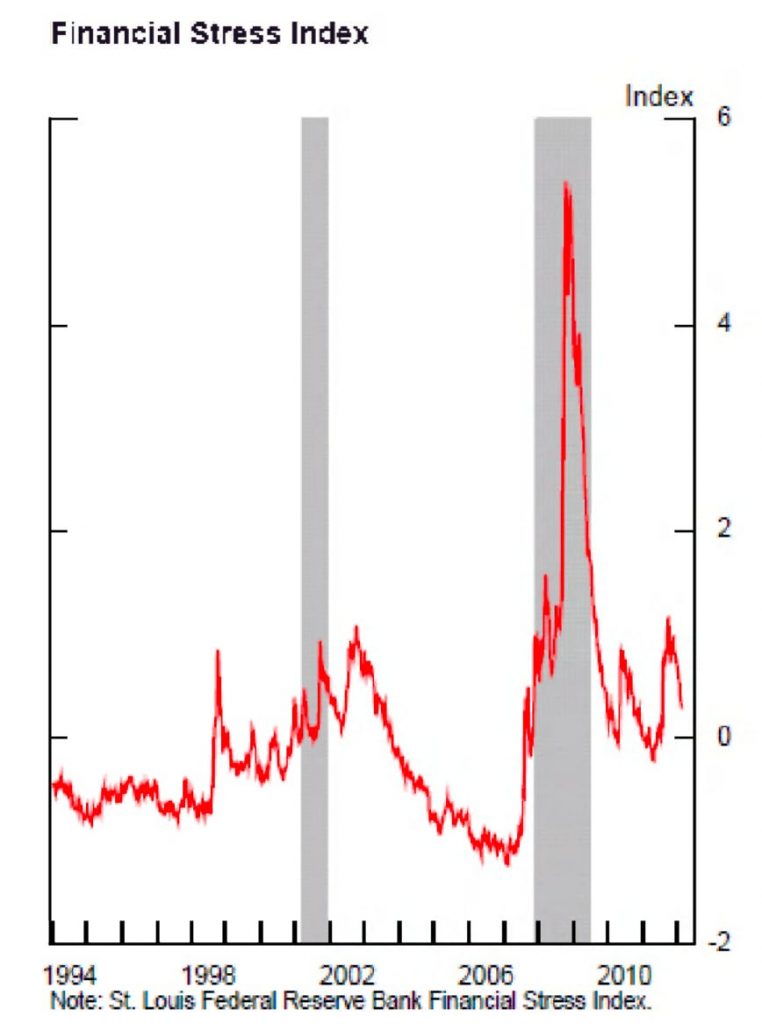

1) Financial stress skyrocketed

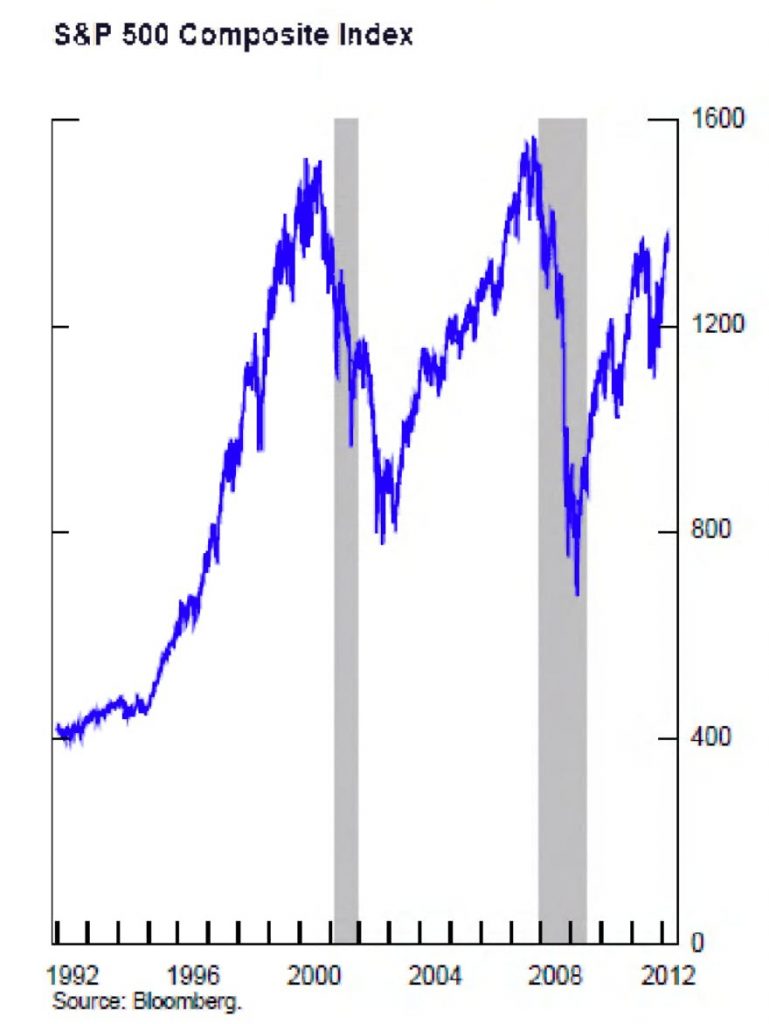

2) The stock market plunged

3) Home construction continued its sharp decline

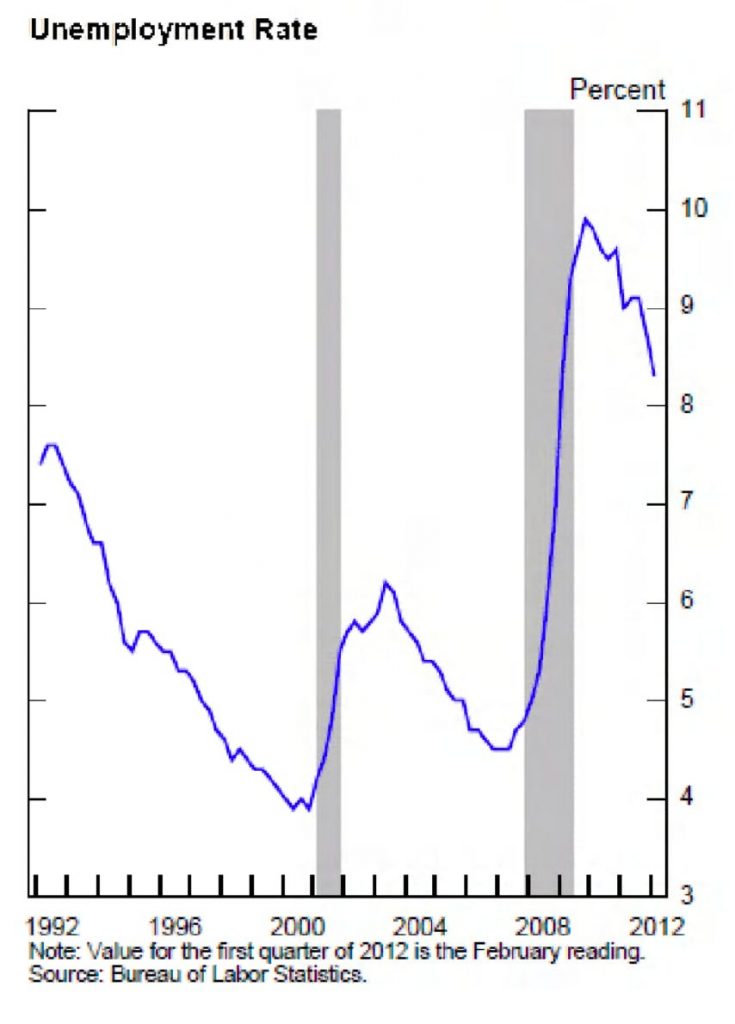

4) The unemployment rate rose sharply

… the list goes on.

The crisis is too big and too complex to summarize in a single lesson, but I hope this gives you the starting point to understand just how complex and intertwined the modern financial system is. If you are interested in digging deeper, I highly encourage you to do more research on your own. The time spent understanding the 2008 financial crisis will help put a lot things (in relation to cryptocurrencies) in perspective for you.

I hope by now that you are starting to understand why a more transparent and less centralized system is necessary for building a resilient economy. The modern financial system is effectively a house of cards waiting to collapse at any moment. There are no checks and balances in place to keep the various actors in check, and so the bankers end up being incredibly greedy and taking big risks knowing that they will always get bailed out by the Fed and government. And this is a big part of what cryptocurrencies hopes to change. It is a monetary system with checks and balances built into the system (i.e. strong incentives).

In the next lesson, we will learn about how the Fed responded to the 2008 crisis (hint: QE).

See you in the next post!

Add Comment