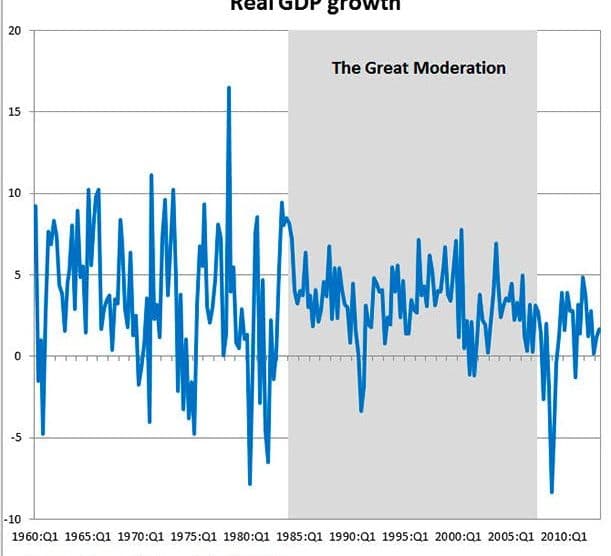

In the last post, we finally read about a period of financial calm in the USA. About time, right? During the Great Moderation, there were still many financial shocks, but they didn’t crash the economy.

At the end of the last post, I left you pondering whether these shocks were too minor to cause a severe recession, or whether the shocks were less severe because the financial system had grown more resilient.

In this post, I will take a look at a number of different shocks to the US financial system from the late ’70s to early 2000s. You’ll see that the US economy faced consequences, but a second Great Depression never resulted. Why? After you’ve read this post, maybe you’ll have some personal theories.

Latin American debt crisis

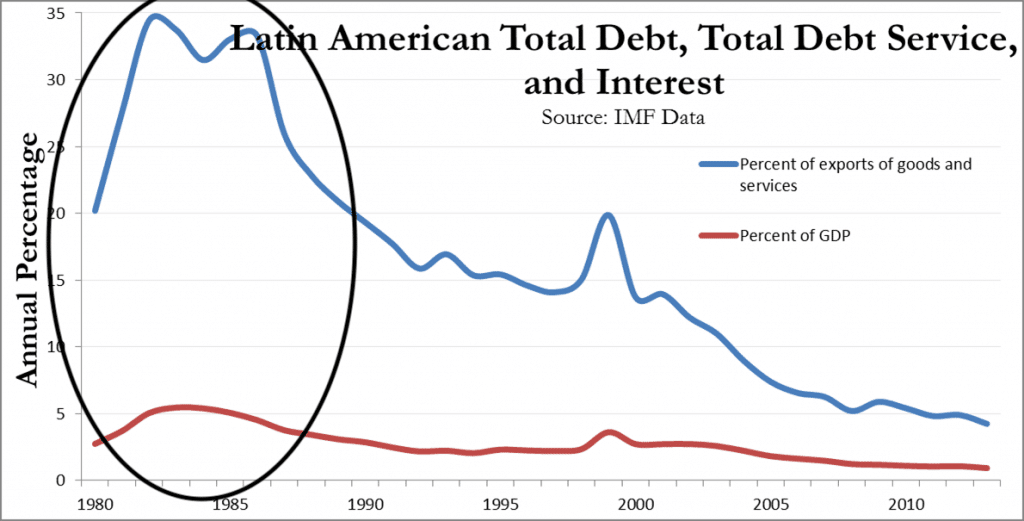

Remember how we learned about the oil crisis during the 1970s? Not only did it have a stark effect on the USA, but the oil price shocks created account deficits in many Latin American countries. Meanwhile, oil-exporting countries were doing well and had account surpluses.

At the end of 1970, Latin American countries’ debt totaled only $29 billion, but by the end of 1978, that number had skyrocketed to $159 billion. By 1982, it reached $327 billion.

At that point, the US decided to step in and “help” by providing the exporting countries that had account surpluses with a safe, liquid place to store their surpluses, and then using these funds to lend to Latin America.

As you may suspect, by lending to Latin American countries, US commercial banks were assuming a lot of risk.

Lo and behold, Latin American countries soon found their debt burdens unsustainable.

Mexico was the first country to tell the US that it was longer able to service its debt. Sixteen other Latin American countries followed suit, as well as 11 other third-world countries.

As the crisis spread, the US tried to help again by restructuring the countries’ debt. Moreover, the International Monetary Fund jumped in and lent these Latin American countries money to at least pay off the interest so that they could avoid defaulting on their loans. Meanwhile, the countries agreed to reform their economies in order to increase their exports so that they could then use that money to pay off the loans.

Desperate to pay off their debt, countries started cutting spending on infrastructure, health, and education, and they froze wages or laid off state employees, which led to high unemployment, steep declines in per capita income, and negative growth. As a result, many Latin American countries entered a deep recession.

Eventually, it became clear that these countries would not ever be able to pay off their debts at the rate they were going. So the US decided to forgive one third of the debt, and in turn, these countries agreed to make additional reforms to pay off the debt down the road. Latin American countries didn’t start to recover from this economic shock for a decade.

Lesson learned?

Clearly US banks overexposed themselves to bad debt, which put the financial system at massive risk. To help save the system, regulators had to weaken regulatory standards for large banks that were exposed to this bad debt in order to avoid a collapse. Banks got a free pass and didn’t face the consequences of their excessive risk-taking. This is one of many examples in US history where banks were bailed out.

Savings and loans crisis

Another “minor” shock to the economy during the Great Moderation was the savings and loan crisis.

S&Ls were thrift organizations established in Pennsylvania in 1831 to help Americans pursue home ownership. An S&L was a group of people who pooled their resources and loaned them to other members to help finance their homes. As the loans were repaid, funds could then be lent to other members.

S&Ls served a big role in the US mortgage market. In 1980, there were 4,000 thrifts with total assets of $600 billion, of which about $480 billion were in mortgage loans.

During the Great Inflation, when Volcker implemented high interest rates to help fight inflation, many S&Ls began to suffer. Instead of letting these S&Ls collapse, the government decided to step in. The government eased regulations to make it even easier to make new residential loans. Many insolvent thrifts were allowed to remain open.

As a result, the S&L industry grew even faster. From 1982 to 1985, the thrift industry assets grew 56%. These institutions went for broke, investing in riskier projects, hoping they would magically pay off in higher returns. Of course, if these returns didn’t materialize and they become insolvent, then guess who footed the bill? Taxpayers! Duh.

As you are undoubtedly expecting, the whole thing came melting down. By 1988, more than 40% of S&Ls had failed. It got so bad that it was cheaper to burn some unfinished condos that a bankrupt Texas S&L had financed rather than try to sell them.

Eventually, Congress decided to address the thrift industry’s problems by instituting a number of reforms to the industry. The main S&L regulator was abolished, as well as the bankrupt Federal Savings and Loans Insurance Corporation (which had served as the insurer for S&Ls). Ultimately, 747 S&Ls with assets of over $407 billion were closed. The ultimate cost to taxpayers was estimated to be as high as $124 billion.

Yikes! And yet, the economy didn’t go under.

The failure of Continental Illinois Bank — the first “too big to fail”

Another shock to the economy occurred in 1984 when Continental Illinois National Bank and Trust Company failed. With $40 billion in assets, the bank was the largest commercial and industrial lender in the United States. This was the largest bank failure in US history (until the 2008 financial crisis). This was when you first started hearing the term “too big to fail.” Or maybe a lesson from the Titanic should have been applied…“unsinkable.” Not quite.

Why did the bank fail?

Simple. The bank made incredibly risky investments, such as purchasing $1 billion in speculative energy-related loans that originated from the 1970s oil and gas exploration boom. When that boom ended, the underlying risk in those loans became apparent, and the bank faced steep losses. The bank had also invested in developing countries like Mexico, who were going through the previously discussed debt crisis in the early ’80s.

By 1984, Continental Illinois Bank’s nonperforming loans went from $400 million to $2.3 billion. When the depositors of the bank learned about this, there were massive bank runs. Of course, the bank wasn’t able to give depositors their money, so it borrowed $3.6 billion from the Federal Reserve. In addition, the bank received a $4.5 billion line of credit from sixteen of the nation’s largest banks.

You may (justifiably!) be wondering why the failing bank was given so much money.

Well, because the banking system is incredibly intertwined. A collapse of the largest bank would likely mean the collapse of the whole system. In this case, 2,300 banks had invested in Continental Illinois. And 179 of those banks had invested more than half of their equity capital in the bank! Moreover, almost half of the invested funds were greater than $100,000 (which is the upper limit for what FDIC insures).

So if the bank failed, it would wreak havoc on the system. Even all this support, though, wasn’t enough to save the bank. So the Fed went even further. The FDIC announced that it would protect creditors with accounts greater than $100,000 (even though this is not what the FDIC is supposed to do) and on top of that, the FDIC infused $1.5 billion capital into the bank.

The bank tried unsuccessfully to find a buyer, and then the FDIC committed to purchasing up to $4.5 billion in bad loans from the bank. In the end, the FDIC protected all bondholders and depositors, while all equity holders were wiped out. The government then bought the bank and held the asset until 1991. In 1994, Bank of America purchased the defunct bank.

I will leave it up to you to figure out whether it was a good idea for the FDIC to provide such unusual support to save a sinking ship. Do you think it would have been better if the bank were allowed to fail? Or was it better to save the bank so that creditors and depositors who didn’t contribute to the problem wouldn’t have to face the consequences? These are important questions to consider, even if they have no easy answers.

Next shock:

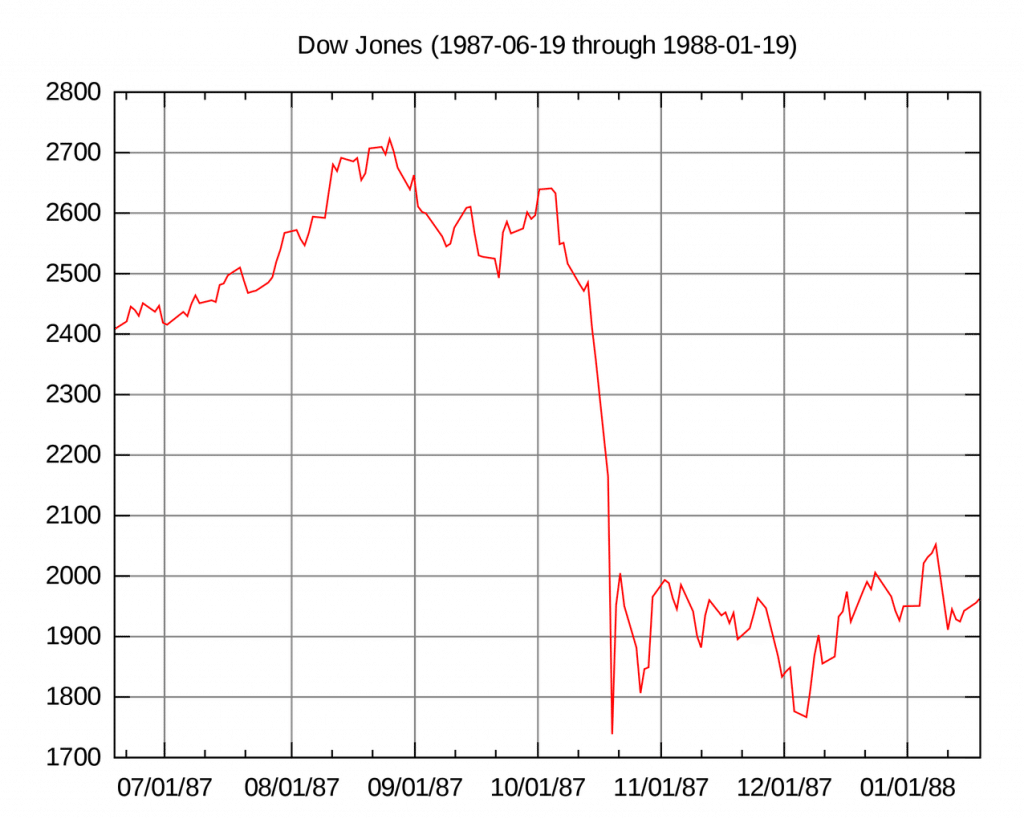

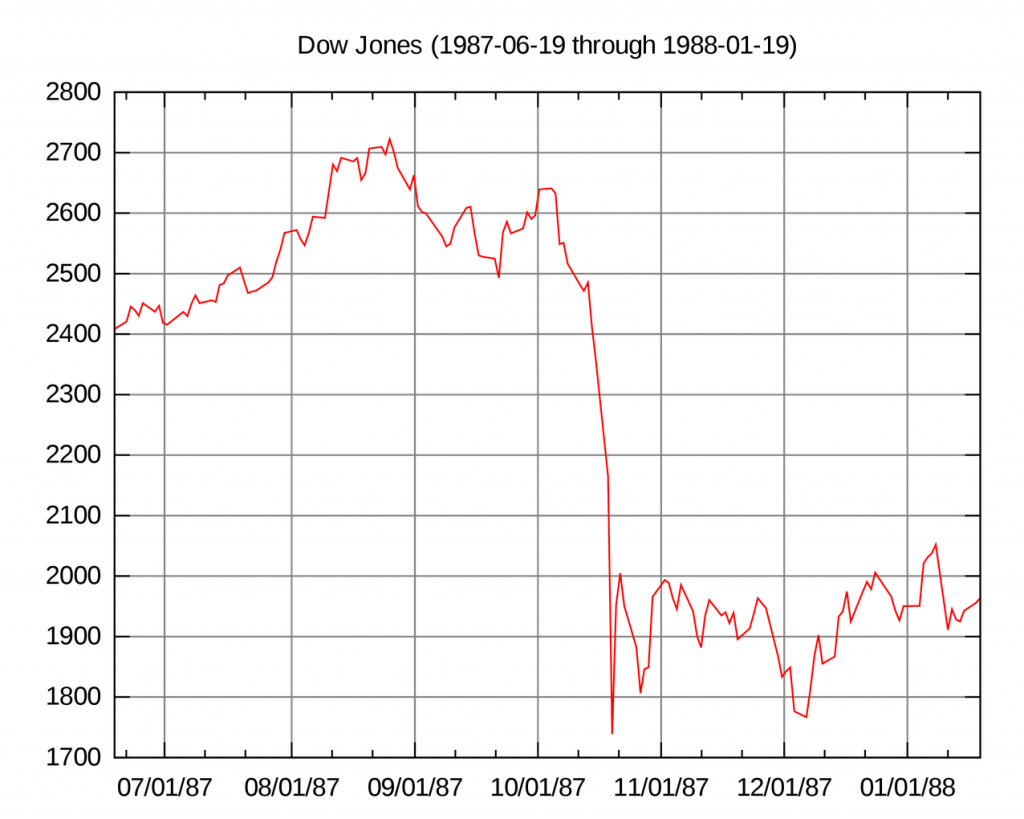

Stock market crash of 1987

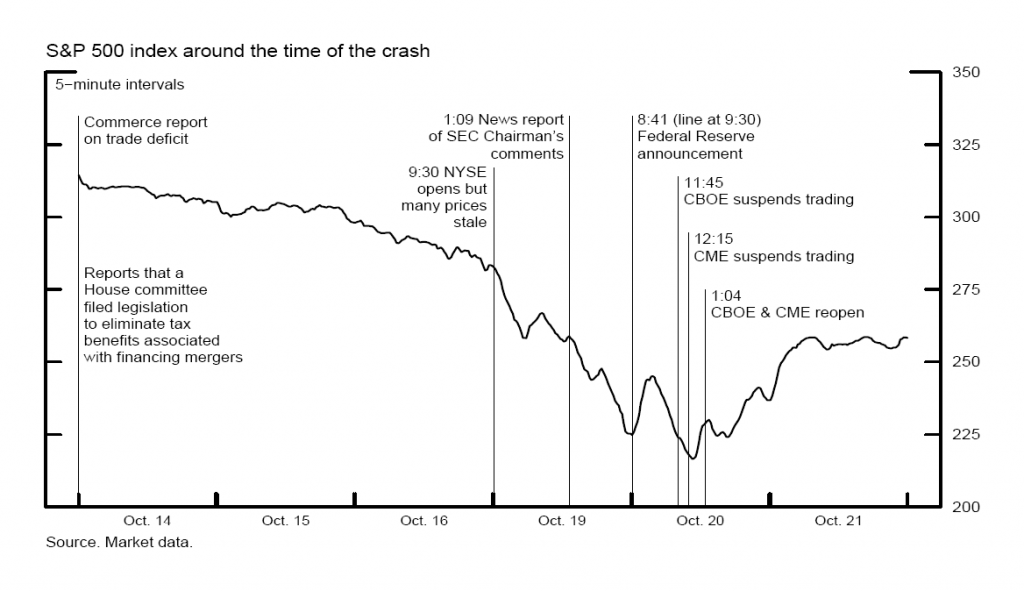

On October 19, 1987, the Dow Jones Industrial Average (DJIA) dropped 22.6% in one trading session. To this day, it remains the largest one-day stock market decline in history, aptly known as “Black Monday.”

The US economic crash caused a chain reaction across global stock exchanges within hours. The financial crisis spread like a virus, from market to market. People stayed up all night to watch the Japanese market, hoping to predict what might happen in the next session of the New York market. It revealed just how interconnected the global markets had become in the decades following the world wars.

“There is so much psychological togetherness that seems to have worked both on the up side and on the down side. It’s a little like a theater where someone yells, ‘Fire!’’

— Andrew Grove, CEO of Intel Corp in New York Times

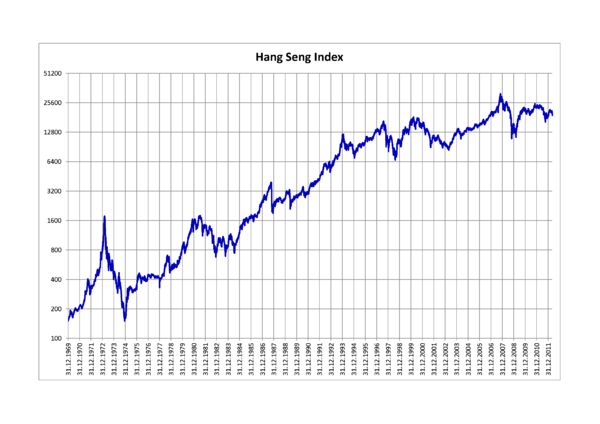

All of the twenty-three major world markets experienced a sharp decline in October 1987, nineteen suffering a decline greater than 20%. Hong Kong, for example, saw a drop of 45.8%.

So what caused Black Monday?

There were a few different causes.

1) Increased investments from international investors in the US market

2) Extensive use of new and complex financial products (e.g., options and derivatives) that had a cascading effect because of how intertwined these financial products were

3) Stock, options, and futures markets used different time lines for the clearing and settlements of trades. This meant some accounts went into negative balances and were forced to liquidate.

How did the Fed respond?

Behind the scenes, the Fed encouraged banks to continue to lend on their usual terms in order to prevent widespread panic and the possibility of bank runs.

Luckily, the strategy worked because there was no economic recession or banking crisis following Black Monday. Within two trading sessions, the DJIA regained 57% of the losses during Black Monday. And within two years, US stock markets surpassed their pre-crash highs.

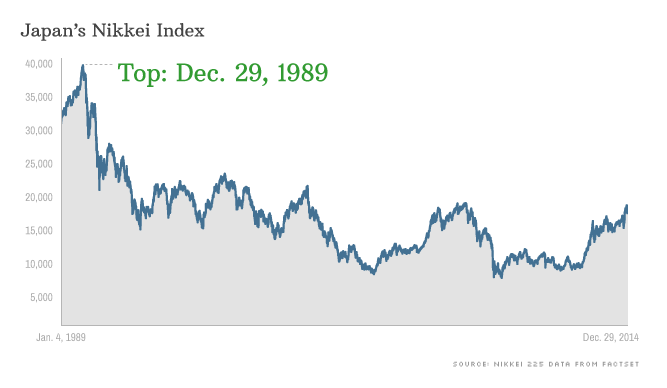

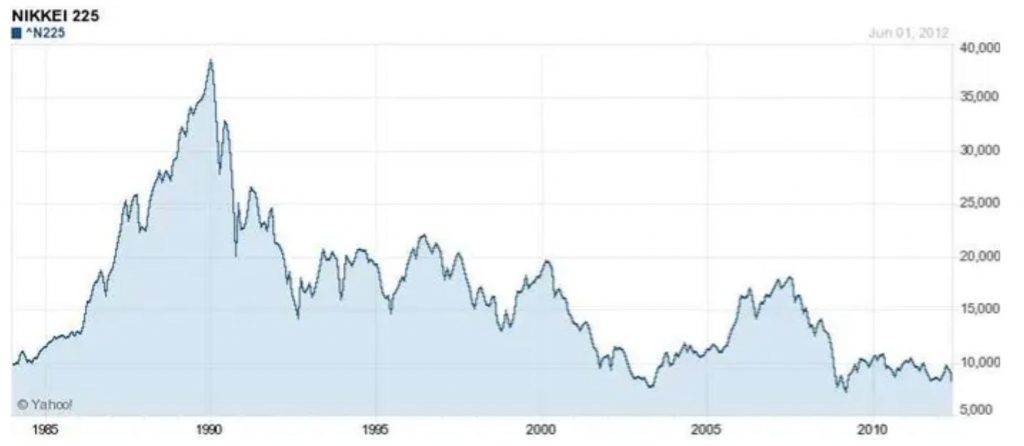

The US was able to swiftly recover over time, but Japan’s economy has been struggling to regain ground ever since.

Now, let’s move onto the next shock.

The Asian financial crisis in 1997

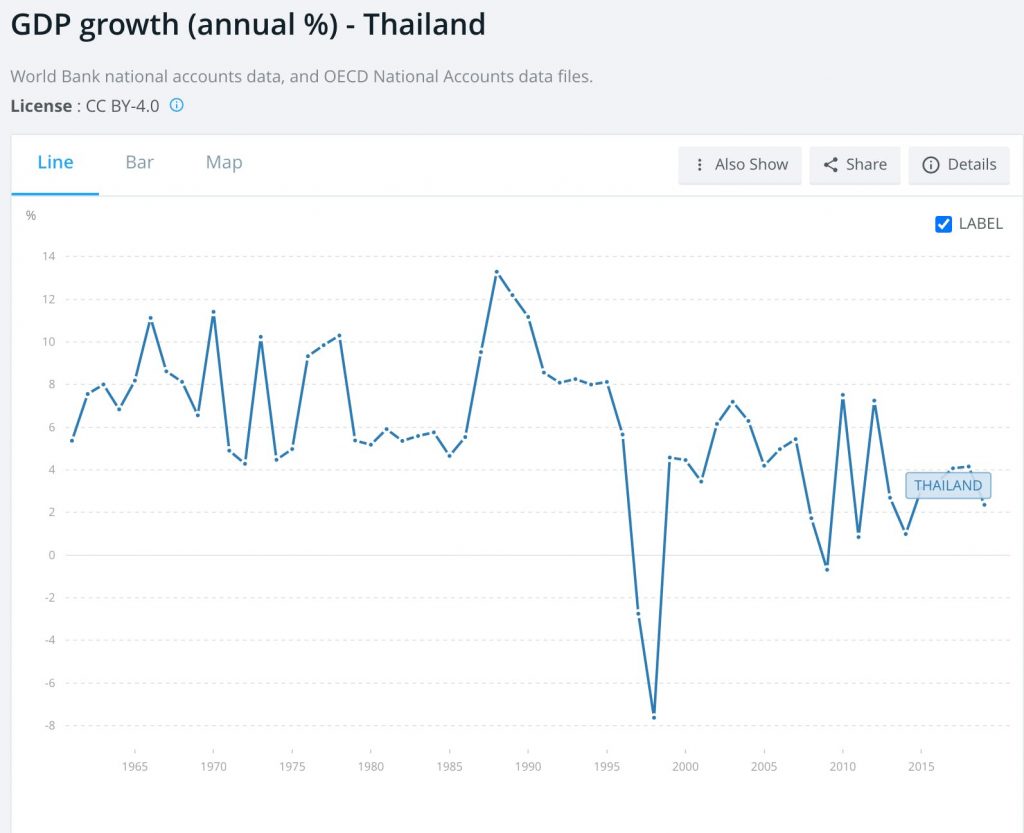

A financial crisis started in Thailand on July 2, 1997, and spread across East Asia, wreaking havoc on local economies. It started when Thailand devalued its currency relative to the US dollar. Thailand was at a balance of payments deficit and the stock and real estate markets were weakening, so the country devalued the currency to save the sinking ship. Malaysia, the Philippines, Indonesia, and South Korea eventually faced the same Asian Financial Crisis.

The global economy was stunned when this happened because prior to the crisis, these countries had seen strong growth rates in GDP.

However, the Asian Financial Crisis revealed that the countries’ rapid growth through risky loans came at a cost of resilience. As these economies started heating up, they started to rely more on borrowing from foreign countries, which exposed the banks to significant amounts of external debt.

The vulnerabilities of the local banking sector had ripple effects, causing foreign creditors to start pulling out, which further escalated the crisis.

The IMF, the World Bank, the Asian Development Bank, and governments in the Asia-Pacific region, Europe, and the United States all came together to mobilize $118 billion worth of loans to Thailand, Indonesia, and South Korea. The goal was to help these countries rebuild their reserves and buy time so that policy adjustments could be made to stabilize and restore confidence in the floundering economies.

The aid was contingent on these countries making policy reforms to clean up and strengthen their financial systems.

What role did the Fed play?

The Fed closely monitored the risks the crisis posed to US banks and encouraged banks to act in their collective self interest in helping these countries avoid a default. For example, US banks decided to roll over short-term loans into medium-term loans. The Fed also helped the Treasury arrange a bridge loan for Thailand in the early stages of the crisis.

Ultimately, the unexpected crisis was contained, and the US did not face a major recession in spite of the economic bump in the road.

Onto the next shock…. I told you this was a long post 😉

The collapse of Long-Term Capital Management in 1998

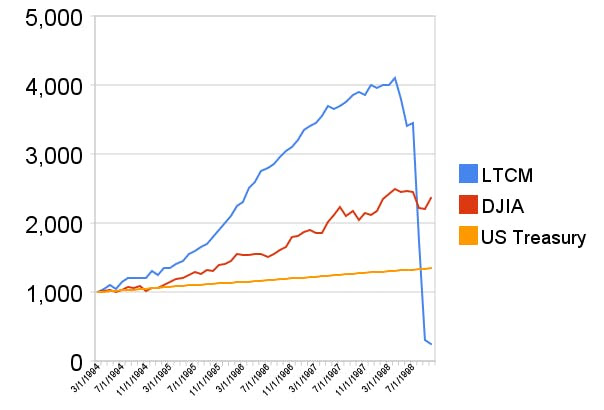

On September 23, 1998, fourteen banks and brokerage firms invested $3.6 billion in Long-Term Capital Management (LTCM) to prevent the firm from collapsing.

LTCM was founded by former Salomon Brothers’ vice chairman John Meriwether in February 1994 and was known to use sophisticated mathematical models to make above-average returns. LTCM generated returns of 20% in 1994, 43% in 1995, 41% in 1996, and 17% in 1997, which was well above average hedge fund returns at the time. LTCM would leverage its positions with debt. And since LTCM had above-average returns, more creditors were willing to loan the company money. By the end of 1997, LTCM was holding about $30 in debt for every $1 of capital.

In 1998, the Asian Financial Crisis started, which motivated investors to move their assets to safer places. At the same time, LTCM’s performance was tanking, and the fund lost 44% of its value in August 1998.

The fund sought out additional capital to stay afloat. When that didn’t work out so well, the fund reached out to the Fed for help.

How did the Fed intervene?

The Fed inspected LTCM and became aware of the dangerous scale and scope of LTCM’s positions. They were afraid that if people started exiting LTCM’s positions, there would be a fire sale that would negatively affect the economy.

The Fed tried to gather four financial firms to come up with a strategy to save the sinking ship. However, they couldn’t agree on an approach. Then Warren Buffet offered to both buy out the firm’s partners for $250 million and inject $3.75 billion into the fund. However, this deal did not go through because of legal issues.

The Fed went back to the drawing board. Eventually, fourteen financial firms agreed to put up $3.6 billion in capital in exchange for 90% ownership of LTCM. The LTCM partners were then required to turn around the ship (with significant oversight) so that they could pay off $3.6 billion, which they managed to do by the end of 1999. The partners and investors of LTCM suffered great losses, but they managed to prevent a collapse of the firm.

In effect, the Fed was able to avoid investing its own funds to save the sinking ship. Instead, it got its creditors to coordinate the rescue plan. If the Fed had invested its own funds, the money would have come out of the pockets of people like you and me, and that would have been very controversial.

It’s worth thinking about why LTCM was allowed to get into such an untenable position. Why should hedge funds be allowed to take such large risks but then get rescued when things go badly? Another question for you to ponder. Yes, there are a lot of them!

And now onto the final shock….

The dot-com crash in 2000

The 1990s were the longest period of economic growth in American history up to that point. In 1993, after Mosaic was invented, people had access to the internet for the first time. Between 1990 and 1997, US households that owned computers increased from 15% to 35%, marking the beginning of the Information Age.

At the same time, interest rates were low so people had capital available to invest. Moreover, the Taxpayer Relief Act of 1997 lowered the top marginal capital gains tax in the United States. This made it even more appealing for the public to invest in stocks. On top of all that, the Telecommunications Act of 1996 was passed, and people expected the telecom industry to then blow up. Telecom companies invested more than $500 billion, mostly financed with debt, into laying fiber optic cable, adding new switches, and building wireless networks.

As a result of cheap capital and a lot of optimism about the internet and telecom, people were eager to invest. There was a lot of irrational behavior and speculative investments being made without much grounding in reality.

But by the end of the millennium, the optimism waned as people started to fear Y2K. You might recall, everyone was scared that computers would have trouble changing their clock and calendar systems from 1999 to 2000. As a result, investments in technology started to get more volatile.

In February 2000, once people realized that Y2K didn’t lead to world apocalypse, the Fed announced plans to aggressively raise interest rates, which made capital more expensive thereby disincentivizing people from investing). Then on March 13, 2000, Japan once again entered a recession, triggering a global sell-off.

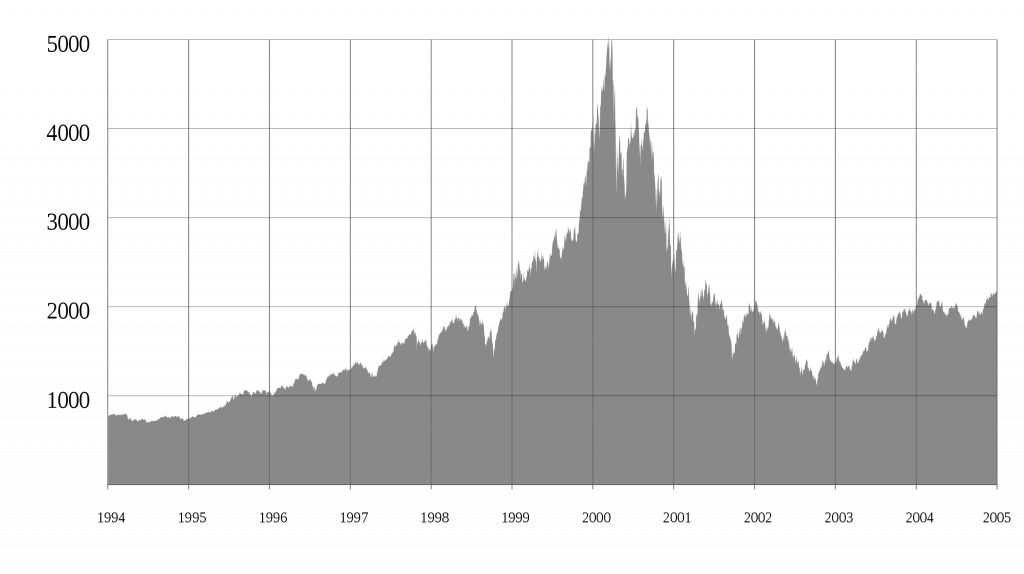

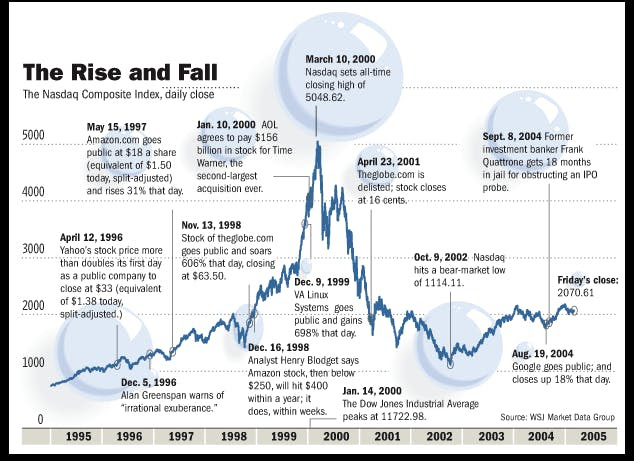

Unfortunately, technology stocks took the hit because people were trying to move their assets from speculative stocks to safer stocks. On March 10, 2000, the NASDAQ Composite stock market index peaked at 5,048.62. What came next was a bloodbath.

News of tech companies collapsing started to scare people. For example, Yahoo! and eBay ended merger talks. Microsoft was found guilty of monopolization and violation of the Sherman Antitrust Act. Pets.com failed; Geocities was acquired by Yahoo but then shut down; Webvan and eToys.com went bankrupt…and the list goes on.

The speculative tech bubble had burst. By the end of 2002, stocks lost $5 trillion in market capitalization. The NASDAQ-100 dropped to 1,114, down 78% from its peak.

The dot-com bubble was yet another shock to the US economy. However, the recession was brief and shallow. It lasted eight months; GDP declined by only 0.3%; and unemployment peaked at 6.3%.

Even though the bubble was pretty bad, the economy was able to sustain the shock without a major recession.

Conclusion

Clearly, there were a lot of shocks in the US economy during the Great Moderation period. However, the economy was resilient and bounced back a lot faster than it did during the Great Depression.

Think about what could have been the cause for this resilience. Is it because the Fed was able to serve as the safety net whenever bad things happened in the economy? Or is it that we just got lucky and the shocks were not as severe as previous shocks? Or was the economy really that much more resilient?

Think about it and let me know in the response.

I’ll see you in the next post, where we’ll talk about the series of events that did finally cause the economy to collapse in 2007. You know it was coming. What goes up must come down.

See you then!

Add Comment